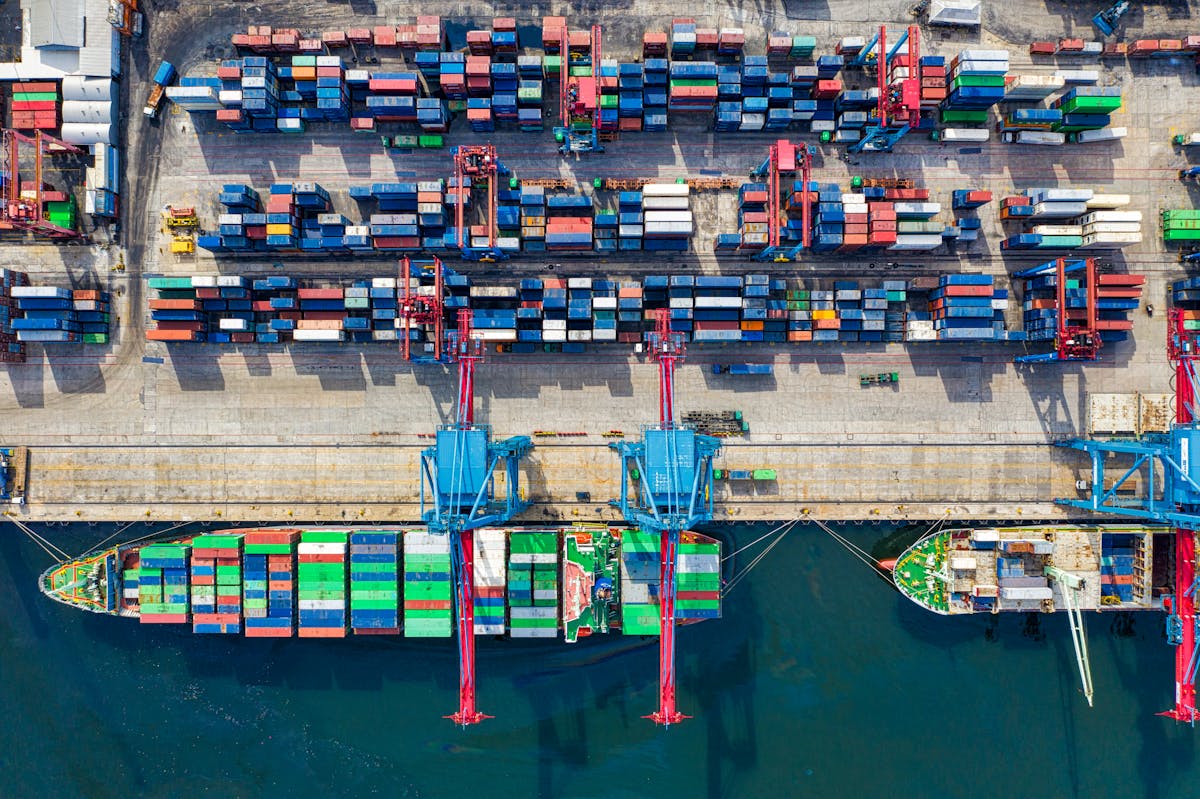

Global supply chains are no longer being reshaped solely by cost optimization, digital transformation, or pandemic-era resilience mandates — they are now being redrawn by treaty signatures, diplomatic ruptures, and strategic export controls. The February 2026 announcement of the provisional EU-India Free Trade Agreement (FTA) — confirmed by European Commission trade officials and validated by India’s Ministry of Commerce — marks a pivotal inflection point. Unlike previous regional trade pacts, this agreement embeds explicit supply chain security clauses, dual-use technology safeguards, and coordinated customs risk profiling mechanisms targeting third-country dependencies. As documented by the World Bank’s latest Global Logistics Performance Index (2025), the EU and India collectively account for 18.7% of global containerized import value, with China supplying $32.4 billion in intermediate goods annually to these markets — primarily electronics components, lithium-ion battery precursors, and precision machining tools.

The Hidden Architecture of the EU-India FTA: Beyond Tariff Cuts

At first glance, the agreement reduces average applied tariffs from 9.3% to 2.1% on over 94% of tariff lines. But its operational impact lies in three structural innovations that directly undermine China-centric logistics networks:

- Preferential Rules of Origin (ROO) Thresholds: Goods must contain ≥55% regional value content (RVC) to qualify — a sharp increase from the ASEAN+3 standard of 40%. Crucially, inputs sourced from ‘non-market economies’ (a term explicitly referenced in Annex IV-B) are excluded from RVC calculations, effectively disqualifying Chinese-sourced semiconductors, optical lenses, and rare-earth magnets even if assembled in India.

- Joint Customs Intelligence Units (JCIUs): Deployed at Rotterdam, Hamburg, Mumbai, and Chennai ports by Q3 2026, these units will share real-time shipment-level data on consignee patterns, bill-of-lading anomalies, and transshipment routing — enabling predictive interdiction of ‘circular trade’ flows designed to mask Chinese origin.

- Strategic Stockpile Coordination Framework: Mandates synchronized inventory reporting for 47 critical inputs (including cobalt cathodes, photolithography resins, and gallium arsenide wafers), with automatic re-routing protocols triggered when stock levels fall below 60-day thresholds — bypassing traditional Chinese distribution hubs like Shenzhen and Ningbo.

This is not trade liberalization — it is geoeconomic zoning. According to a granular analysis by the Rhodium Group’s Supply Chain Integrity Project, implementation of these provisions will reduce Chinese export penetration into EU-India electronics supply chains by 38–44% within 24 months, accelerating relocation of final assembly to Vietnam (projected +22% FDI inflow in electronics), Mexico (targeting nearshoring of EU-bound EV components), and Eastern Europe (Poland’s Wałbrzych Special Economic Zone reporting 14 new Tier-2 auto supplier commitments since January).

Sign up free to read the full article

Create a free account to unlock full access to all articles.

Sign Up FreeAlready have an account? Sign in