Structural Capacity Attrition: From Cyclical Correction to Irreversible Industry Reconfiguration

The February 2026 ACT Research data reveals not a temporary market spike but the crystallization of a multi-year structural inflection point in North American trucking capacity. While spot rates surged more than 20% year-over-year for dry van and approached 25% for reefers, the true significance lies beneath the surface metrics: operating authorities—the legal permits required to operate as a motor carrier—are declining at an accelerating pace, with ACT projecting they will only return to historical norms in early 2026. This is not merely a reflection of short-term economic headwinds; it represents the culmination of sustained, systemic attrition that began in earnest during 2024 and intensified through 2025. Unlike previous downturns where carriers mothballed trucks or paused growth, this cycle has witnessed an unprecedented wave of permanent exits—small fleets dissolving, owner-operators retiring without successors, and mid-sized carriers failing to secure financing for fleet renewal. The root causes are deeply interwoven: persistently negative operating margins in 2023–2024 eroded balance sheets, while regulatory compliance burdens—including the Electronic Logging Device (ELD) mandate’s full enforcement, new CSA safety scoring thresholds, and increasingly stringent state-level emissions rules—raised the operational overhead for marginal players beyond viability. Crucially, this attrition is self-reinforcing: as fewer carriers remain, the remaining ones gain pricing power, which temporarily boosts margins but simultaneously discourages new entrants due to perceived market saturation and high barriers to entry—not just financial, but also logistical and technological. The result is a fundamentally thinner, less elastic supply base. When demand rebounds—as it has in early 2026 following post-holiday inventory replenishment and resilient consumer spending—the system lacks the latent capacity to absorb it smoothly. This is why load-to-truck ratios have surged to multi-year highs: it’s not that shippers are posting more loads per se, but rather that the denominator—the number of active, qualified, and available carriers—is shrinking faster than the numerator is growing. The industry is no longer cycling between surplus and shortage; it is settling into a new equilibrium characterized by chronically tighter capacity and elevated baseline rates.

This structural shift carries profound implications for shipper procurement strategy and long-term network design. Historically, contract rate negotiations were anchored to spot market volatility, with shippers leveraging periods of oversupply to lock in favorable multi-year agreements. That paradigm is now obsolete. With dry van contract rates rising only in the low-single-digit range while spot rates soar, the gap between contracted and spot pricing has widened to historically dangerous levels—creating massive exposure for shippers relying on legacy contracts that lack robust fuel surcharge mechanisms or escalation clauses tied to index-based benchmarks like the DAT National Rate Index. Moreover, the decline in operating authorities directly undermines the foundational assumption of route guide depth—the average number of carriers listed for a given lane. As noted in the data, route guide depth reached 1.33 in December, its most significant increase in several years, and climbed to 1.52 for long-haul shipments (>600 miles). A depth of 1.52 means that, on average, shippers have fewer than two viable options per lane—a level of concentration that severely compromises negotiation leverage and service resilience. In the Northeast, where the deterioration was most acute (worsening by 16.9%), this translates to near-monopsony conditions for carriers, enabling them to cherry-pick high-margin lanes and reject lower-yield, backhaul-heavy movements. Shippers can no longer treat transportation as a commoditized cost center; they must now invest in carrier relationship management, predictive analytics for lane-specific capacity forecasting, and collaborative planning with key partners to co-develop asset-light solutions such as dedicated contract carriage or shared-user networks. The era of ‘set-and-forget’ freight procurement is over.

Climate-Intensified Volatility: Winter Storms as Catalysts, Not Anomalies

The winter storms that swept across the Midwest and Eastern U.S. in January and early February 2026 did not create the freight crisis—they exposed and accelerated pre-existing vulnerabilities in an already stressed network. While weather disruptions are perennial, their impact in early 2026 was magnified exponentially by the confluence of three compounding factors: depleted carrier capacity, heightened equipment utilization, and fragile just-in-time inventory systems. With operating authorities at historic lows and fleets operating at >95% utilization, there was virtually no buffer to absorb the sudden loss of thousands of lane-miles due to road closures, driver hours-of-service (HOS) exhaustion from extended detention, and terminal congestion at key intermodal gateways like Chicago and Newark. The storms didn’t just delay shipments; they triggered cascading failures across interconnected modalities. Rail networks experienced severe delays due to frozen switches and reduced crew availability, pushing more freight onto an already overwhelmed trucking sector. Simultaneously, port operations in Norfolk and Savannah faced labor shortages and equipment unavailability, creating bottlenecks that rippled inland. The result was not a localized event but a continental-scale synchronization of disruption—precisely the scenario that modern supply chains, optimized for efficiency over resilience, are least equipped to handle. This episode underscores a critical strategic blind spot: enterprise risk management frameworks continue to model weather as a low-probability, high-impact event, when in reality, climate change has elevated it to a high-frequency, medium-to-high-impact operational constant. The Intergovernmental Panel on Climate Change (IPCC) projects a 40–60% increase in extreme precipitation events across the U.S. Midwest by 2030, directly threatening the nation’s primary freight corridor. Yet, most shipper TMS platforms lack real-time integration with hyperlocal weather intelligence or dynamic rerouting algorithms that factor in probabilistic storm paths. Instead, decisions remain reactive, manual, and siloed.

From a carrier perspective, the storms laid bare the unsustainable nature of current cost structures and operational models. Elevated insurance premiums—already up 35% year-over-year due to rising accident severity and frequency—spiked further as underwriters recalibrated risk models post-storm. Financing costs, too, tightened, with banks imposing stricter covenants on carriers with routes concentrated in high-climate-risk zones. Most critically, the storms revealed the hidden cost of ‘efficiency’: fleets that had optimized for minimal deadhead and maximum trailer turns found themselves stranded with empty assets in snowbound regions while demand exploded in unaffected markets like the Southwest. This spatial mismatch wasn’t resolved by price signals alone; it required manual intervention, broker coordination, and costly expedited moves—erosing the very margins that higher spot rates were supposed to deliver. The implication is clear: resilience is no longer optional—it is the primary determinant of profitability. Forward-thinking carriers are now investing in predictive telematics that integrate NOAA forecast data with HOS logs and GPS routing to proactively reposition assets ahead of storm systems. They are also diversifying their geographic footprint, deliberately acquiring authority in secondary markets less prone to systemic weather risk. For shippers, the lesson is equally stark: reliance on single-source, single-lane strategies is a liability. Dual-sourcing critical lanes, building regional safety stock for weather-prone corridors, and embedding climate risk scores into carrier scorecards are no longer best practices—they are table stakes for operational continuity. The February 2026 storm sequence wasn’t an outlier; it was the first major stress test of a supply chain architecture designed for a stable climate—and it failed.

Tariff-Embedded Equipment Costs: The Permanent Price Floor Beneath Linehaul Rates

The persistent elevation of equipment costs—now fully embedded in pricing due to §232 tariffs on imported steel and aluminum—is a silent but decisive force reshaping the economics of truckload transportation. While often discussed in policy circles, the operational impact of these tariffs extends far beyond headline import duties; they have fundamentally altered the total cost of ownership (TCO) calculus for every Class 8 tractor and dry van trailer in the North American fleet. Steel constitutes over 70% of a heavy-duty truck’s weight, and aluminum is indispensable in lightweight trailers designed for fuel efficiency. The §232 tariffs, initially imposed in 2018 and repeatedly renewed and expanded, added 25% to the landed cost of imported steel and 10% to aluminum, costs that domestic producers quickly matched to maintain margin parity. The result? New tractor acquisition costs rose 18–22% between 2022 and 2025, while trailer prices increased 27% over the same period. Crucially, these costs are not transitory; they represent a permanent step-change in capital expenditure requirements. Unlike fuel or labor costs, which fluctuate cyclically, equipment costs are amortized over a 7–10 year lifecycle, meaning today’s higher sticker price locks in elevated depreciation, financing, and insurance expenses for the foreseeable future. This dynamic creates a hard floor beneath linehaul rates: carriers simply cannot accept rates below the breakeven point required to cover this structurally higher TCO. Hence, ACT’s projection that long-haul dry van linehaul rates will trough at roughly $1.60 per mile by April or early May is not a sign of impending relief, but rather the market’s recognition of this new minimum viable rate. Below $1.60, even the most efficient, well-managed fleets would operate at a cash-flow deficit on long-haul moves, forcing them to either exit those lanes or absorb losses that undermine long-term sustainability.

This tariff-induced cost floor interacts synergistically with other structural pressures to cement higher rates. Consider the financing environment: with equipment costs up sharply, lenders require larger down payments (now routinely 25–30% vs. 15–20% pre-tariff) and impose stricter debt-service coverage ratios. Insurance underwriters, too, have raised premiums not only due to accident trends but also because higher equipment values mean larger potential loss payouts. The combined effect is a dramatic compression of fleet operating margins—even before accounting for diesel fuel, which remains volatile, or driver wages, which continue to rise in response to chronic shortages. Fleets are thus forced into a brutal triage of capital allocation: do they replace aging tractors to avoid catastrophic breakdowns and maintain CSA scores, or do they invest in telematics and safety tech to reduce insurance costs and improve retention? Most choose the former, delaying the latter and perpetuating a cycle of higher risk and higher cost. From a shipper’s standpoint, this means that traditional cost-containment levers—such as pressuring carriers on rate per mile—are increasingly ineffective. Negotiations must now pivot to value-based discussions: Can the shipper absorb some portion of the fuel surcharge volatility through indexed pricing? Can they commit to guaranteed minimum volumes on specific lanes to justify carrier investment in dedicated assets? Can they co-invest in trailer tracking or predictive maintenance programs that reduce carrier downtime and improve asset utilization? The tariff story is not about protectionism; it’s about the irreversible recalibration of industrial input costs—and the supply chain must adapt its financial architecture accordingly.

Contract vs. Spot Divergence: The Unraveling of Traditional Rate Benchmarking

The widening chasm between spot and contract rates in early 2026—spot rates up 20–25% YoY while dry van contract rates rise only modestly in the low-single-digit range—signals a fundamental breakdown in the traditional mechanisms used to benchmark, negotiate, and manage freight spend. For decades, the spot market served as a leading indicator and pressure valve: when spot rates spiked, shippers would accelerate contract renewals to lock in predictable costs, and carriers would use spot volatility to justify annual increases. Today, that feedback loop is severed. Contract rates are no longer responding proportionally to market fundamentals because the underlying assumptions of the contract model have collapsed. First, the concept of ‘market rate’ itself is fragmenting. With route guide depth collapsing to 1.33 nationally and 1.52 for long-haul, there is no true competitive bidding process for many lanes—especially in secondary markets or complex, low-volume lanes. Contracts are being renewed out of necessity, not negotiation, with shippers accepting incremental increases to avoid the existential risk of zero capacity. Second, the temporal mismatch is growing: most contracts are negotiated 6–12 months in advance, based on forecasts that cannot anticipate the confluence of winter storms, tariff impacts, or sudden carrier attrition. By the time a 2026 contract takes effect, the market conditions that justified its rate may have shifted entirely. Third, and most critically, the risk transfer mechanism inherent in contracts is failing. Historically, contracts transferred volume and timing risk to the carrier in exchange for price stability. But with carriers facing existential threats—from insurance insolvency to regulatory non-compliance—many are unwilling or unable to absorb additional risk. They are inserting ever-more restrictive clauses: minimum shipment volumes, penalties for late tendering, strict detention windows, and exclusivity requirements. This transforms contracts from partnerships into rigid, high-friction instruments that stifle agility.

The consequences extend far beyond procurement spreadsheets. Finance departments, trained to model freight as a linear cost, are struggling to reconcile P&L volatility driven by unanticipated spot purchases needed to cover contract shortfalls. Logistics teams face operational chaos as carriers prioritize high-margin spot loads over lower-yield contractual commitments, leading to missed pickups, delayed deliveries, and strained customer relationships. Meanwhile, the flatbed segment tells an even starker story: flatbed contract rates remain relatively soft compared to historical norms, despite overall market tightness. This anomaly reveals a deeper truth—that ‘the market’ is not monolithic. Flatbed demand is heavily tied to cyclical construction and energy sectors, which remain sluggish, while dry van and reefer demand is buoyed by resilient retail and food supply chains. Thus, rate divergence is not noise—it is signal. It reflects divergent demand drivers, equipment-specific supply constraints (e.g., specialized flatbed trailers requiring different maintenance and driver certifications), and varying degrees of carrier concentration. For shippers, the imperative is to abandon blanket ‘freight rate’ thinking and adopt lane-specific, mode-specific, and equipment-specific analytics. This requires moving beyond ERP-integrated TMS to AI-powered platforms that ingest real-time spot indices, carrier financial health scores, weather forecasts, and macroeconomic indicators to generate dynamic, probabilistic rate forecasts for each unique lane. Only then can procurement move from reactive bargaining to proactive risk mitigation—treating freight not as a cost to be minimized, but as a strategic capability to be optimized.

Carrier Capital Discipline: Strategic Restraint in an Age of Scarcity

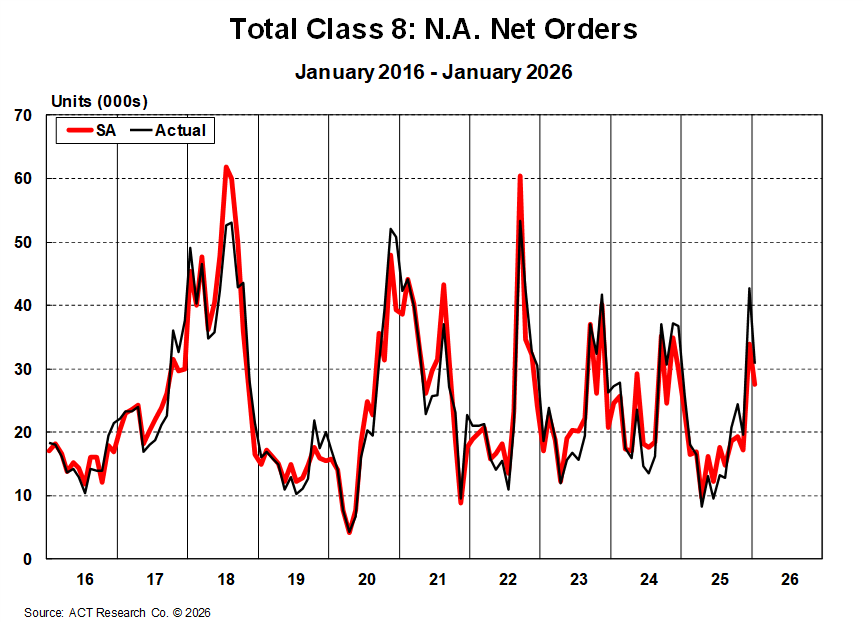

In contrast to the aggressive fleet expansion seen in prior cycles, the carrier response to elevated 2026 rates is characterized by extraordinary capital discipline—a deliberate, strategic restraint rooted in hard-won lessons from the 2022–2024 downturn. Rather than rushing to order new trucks in response to soaring spot rates, fleets are exhibiting remarkable selectivity in capital deployment, focusing intently on replacement timing and asset optimization. This is not conservatism born of caution; it is sophistication born of experience. Carriers now understand that adding capacity in a structurally tight market does not yield proportional returns—it dilutes margins, accelerates equipment depreciation, and invites regulatory scrutiny. The data shows Class 8 net orders remain subdued, a trend corroborated by the chart embedded below, which illustrates the persistent weakness in new truck orders despite record-high rates. Why? Because carriers recognize that the primary constraint is not equipment—it is people. Driver shortages remain acute, with the American Trucking Associations estimating a shortfall of 80,000 drivers in 2026, exacerbated by demographic aging and insufficient training pipeline investment. Adding trucks without drivers is not growth—it is wasted capital. Furthermore, financing for new equipment is more expensive and harder to secure, with lenders demanding stronger balance sheets and clearer path-to-profitability narratives. Insurance providers, too, are tightening underwriting standards, refusing coverage for fleets with poor CSA scores or inadequate safety technology. Thus, capital is being directed not toward expansion, but toward resilience: upgrading telematics for predictive maintenance, installing advanced driver-assistance systems (ADAS) to reduce accidents and insurance premiums, and investing in driver retention programs like improved home-time guarantees and career-path development.

This disciplined approach has profound implications for market dynamics. It means that the anticipated ‘supply response’ to high rates will be delayed, muted, and highly selective—focused on replacing aging, inefficient assets rather than adding net new capacity. Consequently, the market’s elasticity is lower than ever, reinforcing the structural tightness observed in load-to-truck ratios and route guide depth. For shippers, this necessitates a fundamental shift in carrier engagement strategy. The old model of pitting carriers against each other in a race to the bottom is counterproductive; it incentivizes corner-cutting on safety and maintenance, ultimately increasing total cost through accidents, delays, and reputational damage. Instead, leading shippers are forging strategic partnerships with financially healthy, technologically advanced carriers—offering longer-term contracts with built-in performance incentives, co-investing in safety infrastructure, and collaborating on data-sharing initiatives to optimize network flows. These partnerships yield tangible benefits: higher on-time performance, reduced detention, and greater transparency into asset location and condition. In essence, shippers are learning to pay for reliability, not just mileage. The carrier’s capital discipline is therefore not a barrier to shipper success—it is the foundation upon which a more stable, sustainable, and collaborative freight ecosystem can be built. The question is no longer ‘how cheap can we go?’ but ‘how resilient and intelligent can we become?’

Strategic Imperatives for 2026 and Beyond: From Cost Center to Core Competency

The convergence of structural capacity erosion, climate-driven volatility, tariff-embedded costs, and disciplined carrier capital allocation signals an irreversible transition: transportation is no longer a back-office cost center but a core strategic competency that demands executive-level attention, cross-functional integration, and technology-enabled agility. This realization compels a comprehensive reimagining of supply chain leadership. First, the C-suite must dismantle the artificial silos between procurement, logistics, finance, and risk management. Freight spend cannot be managed in isolation when it directly impacts inventory carrying costs, customer service levels, and ESG reporting (e.g., Scope 3 emissions). Second, investment priorities must shift from tactical cost reduction to strategic capability building. This includes deploying AI-driven freight market intelligence platforms that synthesize ACT data, DAT indices, weather APIs, and carrier financial feeds to generate forward-looking capacity heatmaps; implementing blockchain-enabled visibility tools that provide end-to-end, immutable shipment tracking across all modes; and establishing formal carrier development programs that co-fund safety technology, driver training, and decarbonization initiatives. Third, organizations must institutionalize scenario planning—not just for demand shocks, but for systemic shocks like climate events, geopolitical trade disruptions, or regulatory sea-changes (e.g., California’s Advanced Clean Trucks rule). This requires moving beyond static Excel models to dynamic simulation engines that stress-test network resilience under hundreds of plausible futures.

At the operational level, this strategic shift manifests in concrete actions. Procurement teams must evolve from rate negotiators to relationship architects, developing tiered carrier portfolios that balance cost, capacity, technology readiness, and sustainability credentials. Logistics teams must embed real-time decision support into daily workflows, empowering dispatchers to make optimal routing choices based on live traffic, weather, and carrier performance data—not just historical averages. Finance functions must develop new KPIs that measure total landed cost—including risk-adjusted premiums for volatility, carbon taxes, and service failure penalties—rather than simple $/mile. Critically, this transformation cannot be outsourced to third parties alone; it requires deep internal capability building, including upskilling talent in data science, supply chain finance, and sustainability accounting. The February 2026 ACT update is not merely a report on trucking rates—it is a diagnostic snapshot of a supply chain industry undergoing tectonic realignment. Those who respond with incremental adjustments will be outmaneuvered by competitors treating transportation as a source of competitive advantage. The winners will be those who recognize that in an era of permanent scarcity, the ability to move goods reliably, sustainably, and intelligently is not just a function—it is the ultimate expression of organizational strength. The fractured backbone of freight is not breaking; it is being rebuilt—stronger, smarter, and more strategic than before.

Source: actresearch.net