The Exponential Trajectory of Global Warehouse Automation Markets

The global warehouse automation landscape is undergoing a period of unprecedented expansion, signaling a fundamental shift in how supply chains are constructed and managed. Current projections indicate that the global warehouse automation market will reach $29.98 billion by 2026, with expectations to nearly double to $59.52 billion by 2030. This growth is underpinned by a compound annual growth rate (CAGR) of 18.7% between 2024 and 2030, reflecting a robust confidence in automation technologies as essential infrastructure rather than optional upgrades. This trajectory suggests that automation is transitioning from a competitive advantage to a baseline requirement for operational viability in modern logistics. The sheer scale of this financial expansion indicates that stakeholders across the industry are committing significant resources to future-proof their operations against volatility.

Regionally, North America continues to dominate the sector, accounting for 35.6% of global revenue, driven by high labor costs and advanced e-commerce infrastructure. Within this region, the United States market alone was valued at $5.19 billion in 2023 and is projected to surge to $16.6 billion by 2030. This disproportionate growth in North America highlights the intense pressure on US logistics providers to modernize rapidly compared to other regions. The disparity between current valuations and future projections underscores the urgency with which companies are adopting these technologies to maintain service levels amidst rising consumer expectations. As the market matures, we anticipate a consolidation of technology providers who can offer scalable, integrated solutions that meet this exploding demand.

Navigating the Persistent Labor Shortage and Rising Wage Pressures

The primary catalyst accelerating the adoption of warehouse automation is the severe and persistent constraint within the labor market. Labor costs currently consume between 50-70% of warehousing budgets, making workforce management the single largest expense category for most operators. In 2024 alone, warehouse employee wages increased by 7-9%, a rate that significantly outpaces general inflation and puts immense pressure on operating margins. When the majority of a budget is tied to human capital, even modest wage hikes can render traditional fulfillment models economically unsustainable. This financial reality forces executives to view automation not merely as a tool for efficiency, but as a critical mechanism for cost containment and budget predictability in an erratic labor environment.

Beyond the cost implications, the availability of qualified workforce talent has become a critical bottleneck for industry growth. Data reveals that 59% of warehouse managers identify finding qualified workers as their biggest challenge, surpassing even technology integration issues. This scarcity means that even if capital were available to hire more staff, the talent pool simply does not exist to support manual expansion plans. Consequently, automation serves as a force multiplier, allowing existing teams to manage higher volumes without proportional headcount increases. The industry is effectively decoupling revenue growth from headcount growth, ensuring that supply chains can scale to meet holiday peaks and e-commerce surges without being held hostage by recruitment failures.

Strategic Capital Allocation and Budgetary Shifts Toward Technology

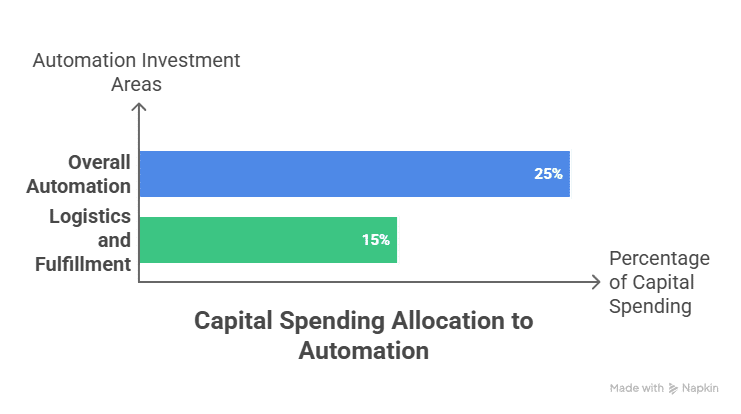

In response to these labor and market pressures, organizations are fundamentally restructuring their capital expenditure strategies to prioritize technology over traditional operational spending. Approximately 60% of companies plan to increase their automation budgets by 20%, signaling a decisive shift in financial prioritization. Furthermore, 25% of all capital spending is now planned specifically for automation over the next five years. This reallocation represents a long-term strategic commitment rather than a short-term tactical fix. By locking in capital for automation, companies are betting on the long-term ROI of machinery and software over the recurring, escalating costs of manual labor. This shift also indicates that automation projects are moving from pilot phases to core infrastructure investments within corporate balance sheets.

The momentum behind this spending is further evidenced by the fact that 68% of enterprises are actively accelerating their warehouse modernization initiatives. This acceleration suggests that the window for being an early adopter is closing, and the industry is moving into a phase of widespread normalization. Companies that delay these investments risk falling behind competitors who achieve lower cost bases and higher throughput speeds. The budgetary increase is not just about buying robots; it encompasses the entire ecosystem including software integration, network infrastructure, and training. As 60% of firms boost budgets, the competitive landscape will likely bifurcate between highly automated, efficient operators and those struggling with legacy manual processes and shrinking margins.

Infrastructure Evolution Through AS/RS and Robotic Integration

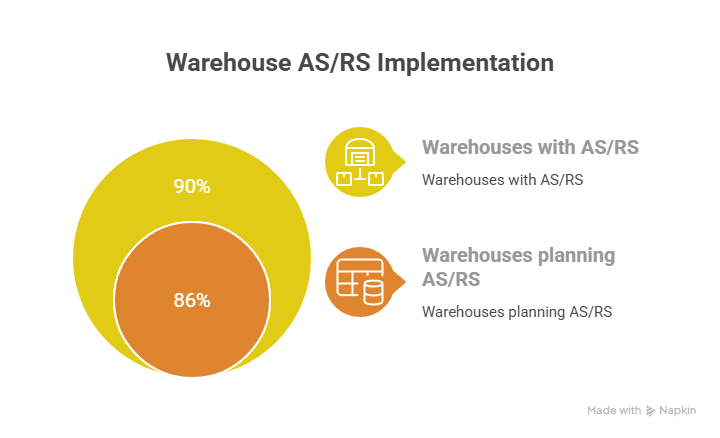

The backbone of this technological transformation is the widespread deployment of Automated Storage and Retrieval Systems (AS/RS), which are becoming the standard for high-density storage and retrieval. Statistics show that 86% of warehouses either already have or plan to deploy AS/RS systems, indicating near-universal acceptance of this technology. Hardware continues to dominate the financial landscape, comprising 58% of global revenue within the automation market. This heavy weighting toward hardware suggests that the physical transformation of the warehouse floor is the primary focus before software optimization takes precedence. The high adoption rate of AS/RS reflects a need to maximize cubic space utilization, allowing facilities to store more inventory within the same footprint, which is crucial as real estate costs continue to climb in logistics hubs.

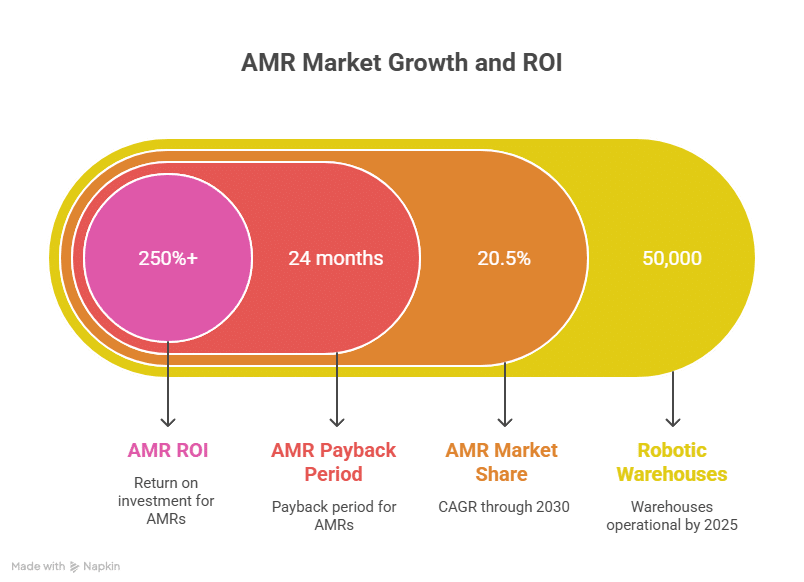

Complementing static storage systems is the rapid proliferation of mobile robotics, with 4.69 million warehouse robots expected to be installed by the end of 2026. The choice between Autonomous Mobile Robots (AMR) and Automated Guided Vehicles (AGV) is critical, with AMRs gaining favor due to their flexibility and lack of need for fixed infrastructure like magnetic tapes.

This shift allows warehouses to reconfigure layouts dynamically based on seasonal demand changes. Additionally, these physical systems rely on robust Warehouse Management System (WMS) architecture to coordinate movements, ensuring that hardware investments are fully utilized through intelligent software orchestration.

Quantifying Operational Efficiency and Return on Investment

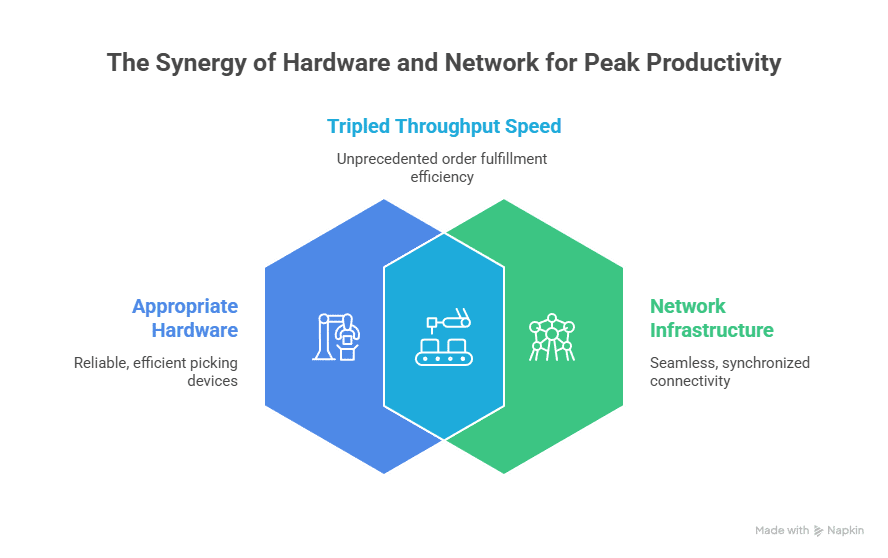

The justification for these massive capital outlays lies in the tangible operational improvements and financial returns that automation delivers. One of the most compelling metrics is the payback period for Autonomous Mobile Robots, which is typically less than 24 months, with an ROI exceeding 250%. Such rapid returns mitigate the risk associated with high upfront hardware costs and provide clear financial visibility for CFOs. Furthermore, automated picking systems have demonstrated a 300% improvement in fulfillment speed compared to manual processes. This tripling of speed is essential for meeting same-day and next-day delivery promises that have become the standard in modern e-commerce. The efficiency gains are not marginal; they are transformative, fundamentally altering the throughput capacity of existing facilities.

Beyond speed and ROI, the impact on overall operating expenses is profound, with 80% of advanced automation warehouses reporting lower operating costs. This reduction is achieved through a combination of reduced labor dependency, lower error rates, and decreased product damage.

When operating costs decline while throughput increases, the margin expansion potential is significant. These metrics validate the strategic pivot toward automation, proving that it is not just a technology upgrade but a financial lever that improves the bottom line. Companies leveraging these technologies are building a cost structure that is resilient to wage inflation and labor shortages.

Long-Term Industry Implications and the 2030 Strategic Horizon

Looking toward the 2030 horizon, the warehouse automation market size projection of $59.52 billion implies a logistics industry that will be unrecognizable compared to today’s standards. The convergence of hardware dominance, with 58% of revenue, and software intelligence will create fully autonomous fulfillment centers capable of self-optimization. The industry is moving toward a model where human intervention is the exception rather than the rule, reserved for complex problem-solving and maintenance rather than repetitive movement. This shift will require a new workforce skill set, focusing on robot supervision and data analysis rather than manual picking. The companies that succeed will be those that view automation as a continuous journey of improvement rather than a one-time installation project.

Ultimately, the data suggests that automation is the only viable path forward for scaling supply chains in the coming decade. With 68% of enterprises accelerating modernization, the competitive bar is being raised permanently. Organizations that fail to invest risk obsolescence, unable to compete on speed or cost with automated rivals. The integration of 4.69 million robots by 2026 is just the beginning of a deeper integration of AI and robotics into the supply chain fabric. As we approach 2030, the distinction between a traditional warehouse and an automated fulfillment center will define market leaders from laggards. The strategic imperative is clear: adapt to the automated future or face diminishing relevance in an increasingly demanding logistics landscape.

Source: thenetworkinstallers.com