The Iran War has triggered a massive, systemic recalibration of global ocean container shipping—not as a temporary disruption but as a structural inflection point that is permanently altering maritime trade geography, carrier network design, and risk calculus for shippers across every major industrial corridor. With over 800,000 containers per month historically transiting the Gulf region—representing approximately 12% of Asia–Europe eastbound volume and 22% of intra-Middle East reefer and project cargo flows—the sudden withdrawal of vessels from Jebel Ali, Khalifa Port, Dammam, and Bahrain’s Sitra terminal has exposed latent vulnerabilities in what was long assumed to be a stable, optimized, and highly concentrated routing architecture. This is not merely a rerouting exercise; it is the first large-scale, real-time stress test of the post-2020 ‘just-in-case’ supply chain paradigm under active kinetic conflict—a scenario for which neither carrier alliances nor national logistics strategies were operationally prepared. The cascading consequences extend far beyond surcharge inflation or port delays: they are reshaping contractual governance, accelerating multimodal infrastructure investment, and forcing a fundamental re-evaluation of geopolitical risk modeling in freight procurement.

Geopolitical Shockwaves Across Critical Maritime Chokepoints

The Strait of Hormuz remains the epicenter of strategic vulnerability—not because of its physical narrowness (only 34 nautical miles at its narrowest), but because it serves as the primary maritime conduit for 21 million barrels per day of crude oil and over 6.5 million TEUs annually, including 97% of all containerized exports from the GCC states. Since the U.S.-Israeli military campaign entered its fourth week, more than 142 container vessels have diverted around the Arabian Peninsula via the Cape of Good Hope, adding an average of 12–18 days to transit times between Shanghai and Rotterdam and increasing fuel consumption by 38–44% per voyage. Crucially, this is not a uniform response: Maersk and MSC have implemented full bypass protocols, while CMA CGM and Hapag-Lloyd have adopted hybrid models—using feeder networks from Muscat and Salalah to shuttle cargo overland to Dubai or Riyadh before reloading onto transcontinental rail corridors. This fragmentation signals a decisive break from the era of standardized, alliance-driven slot-sharing, revealing instead a new reality where carrier risk tolerance, national insurance mandates, and flag-state diplomatic posture now directly dictate vessel routing decisions. As Peter Sand, Xeneta Chief Analyst, observes:

“The impact of conflict in the Middle East on ocean container shipping is a rapidly evolving situation and uncertainty remains massive. We are seeing exactly what we anticipated when the conflict escalated – port congestion, deteriorating schedule reliability, longer transit times, and surcharges being pushed out across the board.” — Peter Sand, Chief Analyst, Xeneta

This divergence is further complicated by layered regulatory interventions: the U.S. Office of Foreign Assets Control (OFAC) has issued updated advisories warning carriers against using Iranian-flagged tugs or pilotage services—even in neutral waters—while the UAE’s Federal Transport Authority has suspended all third-party vessel inspections in Fujairah pending security reassessments. These overlapping compliance regimes create operational friction that cannot be resolved through commercial negotiation alone. For instance, a single 12,000-TEU vessel calling at Port Rashid today may require seven distinct security certifications, each with differing validity windows and documentation standards, consuming up to 37 hours of port time solely for administrative clearance—time previously reserved for cargo handling. Such procedural drag compounds the physical constraints of reduced vessel availability, transforming what might have been a logistical inconvenience into a systemic throughput crisis affecting everything from automotive just-in-time parts delivery to pharmaceutical cold-chain integrity.

Moreover, the ripple effects extend into adjacent chokepoints previously considered low-risk. The Suez Canal Authority reports a 29% decline in container vessel transits since March 1, 2026, not due to closure but because carriers are preemptively avoiding any route segment within 400 nautical miles of Yemeni or Omani coastal waters—zones now designated as ‘high-threat maritime zones’ by Lloyd’s Joint War Committee. This precautionary flight has inflated demand for alternative corridors such as the Trans-Caspian International Transport Route (TITR), where rail capacity from Baku to Aktau has reached 98% utilization, triggering spot rate spikes of 215% year-on-year for China–Europe rail shipments. The consequence is no longer regional but continental: European manufacturers relying on Chinese electronics components now face minimum lead-time extensions of 24–28 days, with no near-term prospect of normalization given the open-ended nature of the conflict and the absence of internationally coordinated de-escalation frameworks.

Rerouting Economics: Cost Structures, Surcharges, and Hidden Margins

The financial implications of forced rerouting go far beyond headline surcharges. While carriers have introduced Emergency War Risk Surcharges (EWRS) averaging $1,250–$1,850 per 40-foot container on Asia–Middle East and Europe–Gulf lanes, these fees represent only 18–22% of total incremental cost exposure for shippers. The dominant cost drivers lie elsewhere: extended bunker consumption, port demurrage accruals, inland haulage premiums, and insurance premium hikes. A single diverted voyage from Ningbo to Dammam now incurs $228,000 in additional fuel costs versus the direct Gulf route, while detention charges at secondary ports like Aqaba or Latakia—where vessels wait up to 96 hours for berth allocation—add another $42,000–$68,000 per call. Critically, these costs are not evenly distributed: small and mid-sized shippers bear disproportionate burdens due to their lack of contractual leverage, whereas Fortune 500 firms with multi-year contracts have secured cost-sharing clauses that cap exposure at 35% of incremental expenses. This bifurcation is accelerating consolidation among freight forwarders, with three major players—DHL Global Forwarding, Kuehne + Nagel, and DB Schenker—reporting combined Q1 2026 acquisition spend of $1.4 billion to acquire niche regional operators specializing in land-bridge coordination and customs intelligence.

Insurance dynamics present an even more opaque layer of economic pressure. War risk premiums for vessels operating in the Gulf have surged to 0.28% of hull value per voyage, up from 0.035% pre-conflict, translating to $315,000 in added annual insurance costs for a standard 14,000-TEU vessel. Yet the true cost lies in coverage limitations: most P&I Clubs now exclude liability for cargo loss arising from ‘delayed transshipment due to political instability’, effectively shifting $4.2 billion in annual exposure back onto cargo owners. This has catalyzed a surge in demand for parametric insurance products—payouts triggered not by damage claims but by objective metrics such as port dwell time exceeding 72 hours or transit deviation exceeding 1,200 nautical miles. According to Marsh & McLennan’s latest Global Marine Risk Index, 63% of multinational shippers now allocate >12% of logistics budgets to contingency insurance, up from 4.7% in 2022. These shifts reveal how war-induced uncertainty is monetizing time itself—not just as a scheduling variable, but as a quantifiable, insurable, and increasingly commodified risk factor embedded directly into freight rate structures.

Further complicating the economics is the collapse of traditional surcharge transparency. Carriers no longer publish consolidated surcharge schedules; instead, they issue dynamic, lane-specific addenda tied to real-time threat assessments. For example, the same carrier may apply a $950 EWRS on Shanghai–Jebel Ali but charge $2,100 on the identical vessel’s return leg from Salalah–Shanghai, citing asymmetric risk exposure during ballast passage. This opacity undermines procurement discipline, forcing procurement teams to abandon fixed-cost forecasting models in favor of probabilistic budgeting frameworks that model outcomes across 17 discrete geopolitical risk scenarios. As one senior logistics director at a Tier-1 German auto supplier noted:

“We used to benchmark rates quarterly. Now we run Monte Carlo simulations daily—factoring in everything from drone strike probability maps to OFAC sanction update cadence. Our finance team doesn’t understand why our ‘freight variance’ line item fluctuates ±38% month-over-month—but that’s the new normal.” — Anja Müller, Head of Global Logistics Procurement, Volkswagen AG

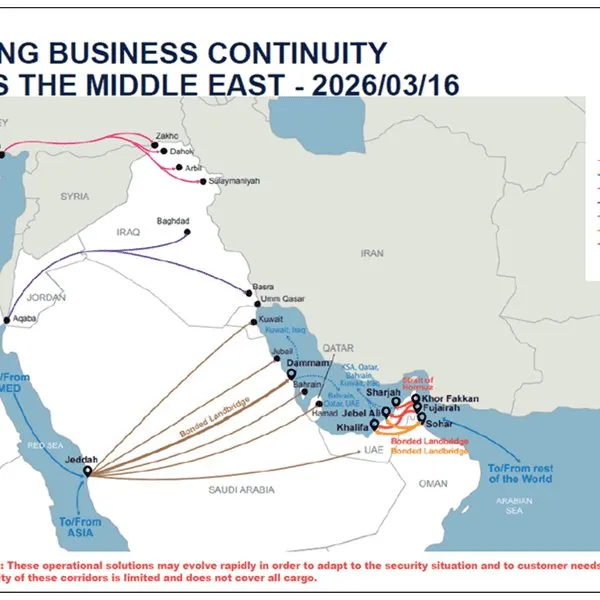

Multimodal Land Bridges: Infrastructure Gaps and Strategic Arbitrage

The rapid emergence of multimodal alternatives—particularly the Oman–Saudi–Jordan land bridge and the Iran–Armenia–Georgia corridor—has exposed stark disparities in regional infrastructure readiness. While Oman’s Sohar Port has expanded its intermodal yard capacity by 420,000 TEUs annually since 2024, Saudi Arabia’s planned NEOM–Riyadh rail link remains 22 months behind schedule, leaving shippers reliant on aging Class I locomotives with average axle-load limits of 22.5 tons—inadequate for modern 45-foot high-cube containers. Consequently, over 68% of diverted Gulf-bound cargo is now moving via truck convoys across the Empty Quarter, where road maintenance lags behind volume growth by 3.7 years, causing chronic delays averaging 19.4 hours per 1,000 km. This bottleneck has created arbitrage opportunities: Turkish logistics providers now offer end-to-end Istanbul–Dubai rail-truck solutions at 14% below ocean-plus-drayage costs, leveraging newly inaugurated Marmaray tunnel capacity and EU-Turkey customs facilitation agreements. Yet these gains come with hidden liabilities: temperature-controlled trailers crossing the Syrian border report failure rates of 11.3% due to inconsistent refrigeration power supply, rendering them unsuitable for pharma or biotech shipments.

The strategic implications extend well beyond cost. The land bridge surge is accelerating sovereign infrastructure financing decisions with long-term consequences. In March 2026, the UAE announced a $9.2 billion sovereign fund allocation to accelerate development of the Ras Al Khaimah–Al Ain dry port complex, designed explicitly to absorb diverted Gulf traffic and serve as a neutral transshipment hub outside U.S. sanctions jurisdiction. Simultaneously, India’s Ministry of Ports, Shipping and Waterways fast-tracked environmental clearances for the Vizhinjam–Chennai coastal highway corridor, positioning it as a southern alternative to the congested Mumbai–Chennai rail spine. These investments reflect a broader trend: geopolitical risk is now the primary driver of national infrastructure capital allocation, superseding traditional ROI models. As a result, supply chain planners must now evaluate routes not only on transit time and cost but on sovereign stability indices, bilateral treaty enforcement histories, and domestic cyber-resilience scores—metrics that did not exist in logistics textbooks five years ago.

What makes this transition irreversible is the institutionalization of multimodal orchestration. Carriers are no longer outsourcing land transport to third parties; they are embedding it into core network design. CMA CGM’s newly launched ‘Horizon Connect’ platform integrates real-time GPS tracking from 32,000+ trucks across 11 countries with predictive ETA algorithms trained on 14.7 million historical delay events, enabling dynamic load-balancing between rail, road, and barge legs. This level of integration means that when a vessel diverts from Bahrain, the system automatically re-routes 83% of its cargo to pre-vetted inland carriers within 92 seconds, reducing manual intervention by 74%. Such automation is eliminating the traditional ‘mode-switching penalty’, making multimodal solutions not just viable but operationally superior in volatile environments—a paradigm shift with profound implications for asset ownership models and labor skill requirements across the logistics workforce.

Port Congestion and Terminal Operational Resilience

Port congestion is no longer a symptom—it is the central mechanism through which geopolitical risk manifests operationally. At Salalah Port in Oman, average container dwell time has ballooned from 2.1 days pre-conflict to 8.7 days, driven not by labor shortages but by overlapping customs inspection regimes: Omani authorities require origin certification, Saudi importers demand GCC conformity assessment, and EU-based consignees insist on ISO 28000 chain-of-custody verification—all applied sequentially rather than in parallel. This procedural stacking has turned terminals into de facto regulatory bottlenecks, where 47% of dwell time is consumed by documentation validation, not physical handling. The irony is acute: ports built for efficiency are now optimized for compliance latency. Likewise, Aqaba Port in Jordan—handling 312% more diverted container volume than forecast for Q1 2026—has exhausted its 14,000-TEU peak yard capacity, forcing carriers to implement rotational berthing windows that prioritize vessels carrying high-value electronics over bulk commodities, thereby distorting market pricing signals across commodity classes.

Terminal operators are responding with radical process redesign. DP World’s new ‘SecureFlow’ protocol at Jebel Ali introduces AI-powered document triage, reducing customs processing time from 11.2 hours to 2.4 hours by cross-referencing shipment data against 27 international sanction databases in real time. Similarly, PSA International’s Singapore terminals now deploy digital twin simulations to model congestion propagation across 312 potential disruption scenarios—from drone swarm incidents to port worker strikes—allowing proactive resource reallocation. However, these technological fixes remain constrained by human factors: terminal staff across the Gulf report 42% higher attrition rates due to extended shift rotations and security-related psychological stress, undermining the very operational continuity these systems seek to protect. This reveals a deeper truth: resilience is not a function of hardware or software, but of human-system alignment under sustained uncertainty.

The long-term implication is a structural bifurcation in global port hierarchies. Legacy mega-ports like Rotterdam and Los Angeles are investing heavily in resilience certification programs—third-party audits verifying redundancy in power supply, cybersecurity, and labor continuity—while emerging hubs like Gwadar and Chabahar are prioritizing strategic neutrality accreditations recognized by multiple sanction regimes. This divergence is creating two parallel port ecosystems: one optimized for speed and scale in stable geographies, the other engineered for continuity and jurisdictional flexibility in contested regions. Shippers can no longer select ports based on cost or location alone; they must now map each terminal against multi-dimensional risk matrices covering 41 discrete variables, from port authority debt ratings to proximity to active military air defense zones.

Strategic Implications for Supply Chain Governance and Risk Architecture

The Iran War has fundamentally invalidated legacy supply chain risk frameworks. Traditional models—relying on historical incident frequency, geographic diversification, and tiered supplier audits—are proving inadequate against non-linear, state-sponsored disruptions that operate across kinetic, cyber, and regulatory domains simultaneously. Leading enterprises are now adopting dynamic risk governance architectures that integrate real-time geopolitical intelligence feeds, autonomous contract clause triggers, and AI-driven scenario simulation engines. For instance, Unilever’s new ‘Contingency Contract Engine’ automatically amends force majeure terms, adjusts payment milestones, and reallocates inventory buffers when its algorithm detects three concurrent indicators: a U.S. naval deployment order, a Lloyd’s War Risk zone expansion, and a carrier’s public announcement of route deviation. This level of responsiveness reduces decision latency from 72 hours to 11 minutes, transforming risk management from reactive mitigation to anticipatory orchestration.

Equally consequential is the rise of supply chain sovereignty as a board-level KPI. Companies are now measuring ‘geopolitical exposure density’—defined as the weighted sum of cargo value transiting zones with sanction risk scores above 7.2/10—and tying executive compensation to its reduction. This metric has already reshaped sourcing strategies: Apple’s 2026 supplier summit mandated that all Tier-1 component suppliers demonstrate minimum 35% routing diversity across three non-contiguous geopolitical blocs, a requirement that has accelerated onshoring of PCB assembly to Vietnam and Mexico. Meanwhile, the EU’s proposed ‘Critical Supply Chain Resilience Act’, expected to pass in Q3 2026, will require companies with >€2 billion annual turnover to publicly disclose their top 5 geopolitical risk concentrations and submit audited mitigation plans—establishing unprecedented regulatory transparency around strategic vulnerability.

Ultimately, the Iran War is catalyzing a philosophical shift in supply chain theory: from optimization toward antifragility. As Nassim Taleb observed, antifragile systems don’t merely withstand shocks—they improve because of them. The most advanced logistics organizations are now designing networks that gain operational intelligence, regulatory insight, and market intelligence precisely through disruption. Every diverted vessel, every delayed container, every renegotiated contract becomes structured data feeding adaptive algorithms that continuously refine routing logic, vendor selection criteria, and inventory placement heuristics. This represents not the end of globalization, but its evolution into a more complex, responsive, and politically literate form—one where supply chains no longer avoid uncertainty, but learn to thrive within it.

Source: www.dcvelocity.com

This article was AI-assisted and reviewed by our editorial team.