The Era of Scarcity: Restructuring Global Networks in 2026

As 2026 unfolds, supply chain professionals find themselves navigating an unprecedented convergence of shortages, soaring costs, and transforming trade dynamics. From ubiquitous raw material scarcity to highly specialized semiconductor bottlenecks, conventional procurement playbooks rooted in just-in-time methodology are crumbling. Resilience is no longer merely a corporate buzzword but an operational prerequisite determining survival in key sectors—ranging from automotive to medical life sciences.

Following the significant disruptions triggered by widespread tariffs and the weaponization of trade policies aimed at national security and compliance, the immediate corporate response centered heavily on inventory accumulation. Yet, top consulting executives indicate that the focus has sharply pivoted from mere disruption management toward the holistic architectural redesign of global networks. Sourcing strategies now prioritize long-term stability and supplier synergy over immediate cost efficiency.

In this new landscape, inventory buffers are being pushed forward aggressively across varying tiers of the supply chain. This deliberate buildup, while mitigating short-term supply shocks, dramatically amplifies holding costs.

- Organizations are rationalizing their active SKU portfolios to mitigate exorbitant price hikes in underlying components;

- Logistics networks have transformed into defensive fortresses prioritizing stock visibility;

- The foundational shifts occurring today are redefining what constitutes a sustainable operational margin.

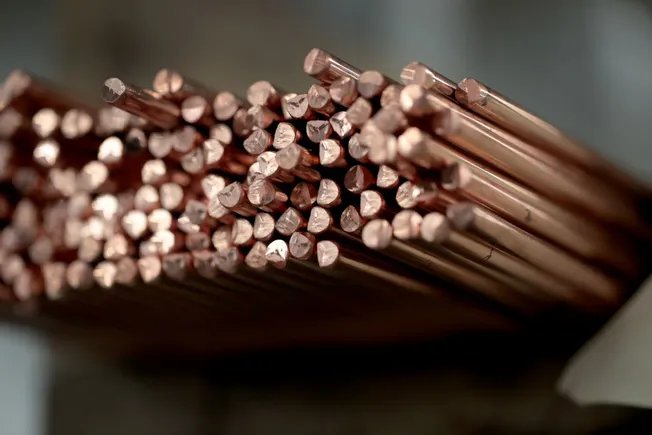

The Copper Squeeze: How AI Centers and Tariffs Stifle Base Metals

The foremost foundational crisis facing supply chains in 2026 is an acutely severe and sustained shortage of refined copper. Driven by a seemingly insatiable global demand for artificial intelligence data centers, advanced electrical infrastructure, and electric vehicle proliferation, copper has swiftly transitioned from a basic commodity to a hyper-strategic asset. Financial analysis from institutions like J.P. Morgan alarmingly project that the United States alone faces a 330,000 metric ton deficit in refined copper this year, propelling base prices well over the $12,000 per metric ton threshold.

Compounding this baseline supply constraint are aggressive geopolitical tariff structures severely impacting global trade flows. The imposition of historic 50% levies on semi-finished copper and copper derivatives by the Trump administration, paired with looming prospective tariffs of 15% on refined copper imports, has triggered panic procurement behaviors. In an environment lacking viable material substitutes for highly conductive metal components, corporations have entered a bidding war where premium capital deployment dictates market access.

This reality is intrinsically tied to production concentration risks spanning a narrow corridor of mining nations. The centralization of refining capacity endows producers with an exaggerated degree of pricing authority, radically restricting the open spot market available to middle-tier manufacturers.

- Massive proportions of output are increasingly locked in extended offtake contracts exclusively with global conglomerates;

- The disruption extends deep into secondary markets resulting in cascading delays for downstream electrical assemblies;

- Logistics professionals operate within hyper-volatile pricing environments where material acquisition eclipses freight efficiency concerns.

Critical Minerals under Siege: Export Controls and Strategic Vulnerabilities

The integrity of advanced technological production, encompassing defense systems, energy transitions, and consumer electronics, hinges precariously on a global supply of critical minerals that is fundamentally insecure. In 2026, the stark reality of Western dependency on complex mineral refining—primarily bottlenecked through strategic competitors—has materialized into acute operational disruptions. The profound structural dependencies established over decades remain stubbornly resistant to rapid geographic decoupling or nearshoring initiatives.

Geopolitical maneuvering has weaponized global supply availability, vividly demonstrated through China’s tightening export restrictions encompassing strategic resources like graphite, antimony, and diverse rare earth elements. These trade barriers function as retaliatory instruments within a broader spectrum of technological containment strategies, effectively stripping end-users of raw material supply security. The ensuing disruptions send shockwaves through procurement forecasts, obliterating predictable cost paradigms.

For strategic sourcing departments, this mineral squeeze represents an intractable challenge that cannot be resolved solely through diverse supplier engagement.

- Alternate global deposits often lack the environmentally intensive processing infrastructure required to produce universally acceptable material grades;

- Extended delays in permitting and developing local extraction environments further stall the bridging of this immediate critical deficit;

- Global players are involuntarily pushed to internalize significant ‘geopolitical risk premiums’ into their extended production budgets.

Surgical Disruptions: Exploding Costs in Medical Supply Chains

The healthcare and pharmaceutical sectors are confronting profound supply chain strains driven concurrently by relentless inflation and concentrated global manufacturing capacity. According to advanced procurement forecasts modeled by industry analysts, medical and surgical equipment inflation is steadily pacing above the 2.58% annual tier, while specialized drug supply costs breach significantly higher margins. This persistent inflation heavily distorts hospital expenditure modeling and limits the acquisition of critical inventory safety stock.

Beneath the surface of pricing volatility lies a structural vulnerability predicated upon highly centralized, single-point-of-failure manufacturing ecosystems. Due to stringent regulatory mandates and validation requirements, the production ecosystem for specific life-saving devices or highly specialized injectable drugs is often isolated to singular certified facilities across the globe. Whether hampered by labor disputes, localized power constraints, or logistical embargoes, any disruption in these critical nodes reverberates immediately throughout global healthcare networks.

Exacerbating the supply deficit are structural shifts in the pharmaceutical development pipeline emphasizing complex, heavily engineered specialty medications over scalable generic staples. Because these products demand rigid temperature-controlled logistics paired with scarce active pharmaceutical ingredients (APIs), the margin for disruption is virtually nonexistent.

- Hospitals are transitioning from standard inventory metrics to building fortified resilience reserves irrespective of capital commitment;

- Contract manufacturing organizations face insurmountable capacity constraints blocking scalable expansion;

- The cumulative impact severely compromises the system’s foundational responsiveness required to handle concurrent global health peaks.

DRAM Famine: The AI Takeover Defunding Automotive Sourcing

While the automotive sector spent the immediate post-pandemic era wrestling with legacy semiconductor limitations, 2026 presents a vastly mutated, highly specialized iteration of the silicon crisis. The core component under immense strain has shifted distinctly to Dynamic Random Access Memory (DRAM). Driven aggressively outward by exponential bandwidth requirements for next-generation intelligence data centers, primary chip fabricators have reallocated massive tranches of their wafer capacity toward AI server memory production margins.

Automotive Original Equipment Manufacturers (OEMs) and Tier 1 electronics suppliers are now relegated to competing against multi-trillion-dollar tech titans for basic wafer allocation. Industry analytics firm S&P Global Mobility projects that base DRAM procurement prices for automotive implementations will skyrocket between 70% and 100% in a remarkably compressed timeframe. This environment starkly transforms the semiconductor dynamic from an exercise in scalable volume acquisition to an uncompromising bidding war for survival capacity.

Furthermore, the automotive sector faces an irreversible cliff edge regarding obsolete technological architecture.

- Primary silicon foundries are rapidly decommissioning legacy DRAM production lines which carmakers have historically depended heavily upon for scalable, cheap processing capability;

- Lead times for placing foundational orders for remaining legacy modules now exceed a debilitating 58-week horizon;

- Faced with forced technological migration and hyper-inflated costs, automakers must rapidly overhaul their baseline computing configurations entirely to prevent devastating assembly line shutdowns.

Livestock Logistics: Climatic Crises Stalling the Agricultural Conveyor

While silicon and essential minerals command significant technological focus, foundational biological supply chains, explicitly within agriculture and food manufacturing, are enduring simultaneous existential constraints. Entering 2026 following a historic 75-year nadir in established cattle herds, food processors and logistics entities face acute meat commodity shortages intricately tied to climatic volatility and prolonged systemic drought conditions across critical grazing topographies.

The systemic reduction in production capacity cannot be remedied through rapid capital injection or expedited fulfillment mechanisms. Cattle raisers natively respond to environmental scarcity by retaining young female livestock strictly for breeding restitution rather than allocating them to standard processing cycles. Agricultural sector analyses reliably predict that overall beef production will persistently compress by an additional 1% across 2026, locking in an unyielding cycle of commodity constraint.

Additionally, compounded challenges including bio-security threats spanning national borders have resulted in extensive livestock import restrictions, severely curtailing nearshored supply networks across the Americas.

- Retail pricing models have fractured beneath the compounding weight of fundamental supply depletion, cascading cost responsibilities aggressively downstream;

- Food logistics managers are constrained from standard inventory buffering due to strict deterioration timelines attached strictly to perishable transit networks;

- Ultimately, prolonged agricultural scarcity mandates structural recalstrations representing an uncharacteristically rigid sector where resilience strategies are dictated completely by ecological recovery rhythms.

Source: Supply Chain Dive