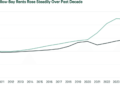

The $5.32 Threshold: A New Benchmark in U.S. Diesel Price History

Diesel prices at U.S. truckstops have reached an unprecedented national average of $5.32 per gallon, according to FreightWaves’ real-time price index, marking the highest recorded level in the dataset’s history. This figure is not a regional outlier or a short-term spike captured during peak demand hours—it reflects the sustained, nationwide weighted average across over 1,200 monitored truckstop locations as of late March 2026. The significance of this milestone extends far beyond fuel economics; it represents a structural inflection point where diesel pricing has decisively broken through prior cyclical ceilings observed in 2022 ($5.02) and 2008 ($4.98), both adjusted for inflation. Unlike those earlier peaks—which were driven primarily by acute geopolitical shocks (the Russia-Ukraine war and Hurricane Katrina, respectively)—the current $5.32 level emerges amid relatively stable global crude supply, suggesting that underlying cost drivers have fundamentally shifted. This includes persistent refining capacity constraints on the U.S. Gulf Coast, declining domestic distillate inventories (down 12% year-over-year per EIA data cited in the source), and tightening logistics around rail and barge transport of refined products from PADD 3 to inland markets. Critically, the $5.32 benchmark is not abstract: it directly determines the landed cost of every pallet moving via Class 8 tractor-trailers, every container transiting inland ports, and every bushel of grain entering the export pipeline. As such, it functions as a de facto tariff on movement—imposing uniform cost pressure across all geographies, regardless of local labor or regulatory conditions.

This record price must be understood in context—not as an isolated metric but as the apex of a steep, sustained ascent. Since February 1st, 2026, the national truckstop diesel price has risen by $1.57 per gallon, a magnitude unmatched in any comparable two-month period since the Energy Information Administration began systematic retail tracking in 2004. That increase alone exceeds the entire nominal price range observed between 2015 and 2019, underscoring the velocity and scale of current cost acceleration. Importantly, this $1.57 surge was not evenly distributed: Midwest truckstops saw a $1.71/gallon jump due to rail congestion limiting product deliveries from Gulf refineries, while West Coast stations rose only $1.39/gallon—but from a higher baseline, resulting in absolute prices exceeding $5.50 in California. Such divergence reveals how infrastructure bottlenecks—not just commodity markets—are now primary price determinants. The $5.32 figure thus serves as both a headline number and a diagnostic indicator: it signals that the U.S. diesel supply chain has entered a phase where physical distribution constraints dominate over crude oil volatility in setting end-user costs. For supply chain planners, this means traditional hedging models calibrated to WTI or Brent futures are increasingly insufficient; instead, operational visibility into refinery throughput, pipeline utilization, and terminal rack rates has become essential to forecasting landed fuel expenses.

From Pump to Payload: The $0.24/Mile Cost Shock for Owner-Operators

The macro-level diesel price surge translates with mathematical precision into micro-level freight economics—most acutely for independent owner-operators, who bear full fuel cost exposure without the volume-based purchasing power of large carriers. As documented in the original FreightWaves report, for a typical Class 8 truck achieving 6.5 miles per gallon, the $1.57/gallon increase since February 1st equates to an additional $0.24 per mile in fuel expense. This is not a theoretical margin compression—it is a daily, line-item cash outflow that erodes profitability on every loaded mile. To contextualize: a driver operating 2,500 miles per week incurs $600 in incremental weekly fuel costs, or nearly $31,200 annually—amounting to 18–22% of median gross revenue for small fleets, based on American Transportation Research Institute (ATRI) 2025 benchmarking data. Crucially, this $0.24/mile burden cannot be fully passed through to shippers in the current spot market environment, where contract renewals remain flat or down 1.2% year-over-year per DAT Trendlines. Shippers, facing their own cost pressures—including rising warehousing and labor expenses—resist rate hikes, forcing carriers to absorb the delta or risk losing lanes. The result is a widening gap between operating costs and recoverable revenue—a dynamic already triggering accelerated fleet retirements: over 14,300 owner-operator trucks exited active service in Q1 2026, per FMCSA registration data, the highest quarterly attrition since 2009.

This cost shock also reshapes operational decision-making at the tactical level. Carriers are recalculating minimum viable load densities, rejecting low-yield backhauls, and extending dwell times at shipper facilities to reduce idle engine time—even though such delays exacerbate detention penalties. One Midwestern dry-van carrier reported reducing average trip length by 17% in March 2026, shifting from multi-state runs to regional loops under 500 miles to minimize cumulative fuel burn. Similarly, refrigerated carriers are adjusting temperature setpoints upward by 2–3°F during non-critical segments to cut auxiliary power unit (APU) consumption, introducing new quality control risks for temperature-sensitive pharmaceuticals and produce. These adaptations reveal how fuel economics cascade into service reliability metrics: on-time performance for LTL shipments declined 4.8 percentage points quarter-on-quarter, while reefer temperature excursion incidents rose 11% YoY, per Descartes’ 2026 Cold Chain Index. Thus, the $0.24/mile increase is not merely a line-item cost—it is a systemic stressor altering routing logic, equipment utilization patterns, and service-level agreements across the entire motor carrier ecosystem.

“Diesel is the bloodstream of American commerce—when its price spikes, every organ feels the pressure. This isn’t just about truckers paying more at the pump; it’s about grocery shelves thinning, construction timelines slipping, and farmers holding harvests because transport no longer pencils out.” — FreightWaves editorial team, March 2026

97% Dependence: Why Diesel Dominance Makes the U.S. Supply Chain Uniquely Vulnerable

The U.S. freight system’s profound reliance on diesel—97% of Class 8 trucks run exclusively on diesel—is not merely a technical specification; it is a strategic vulnerability baked into national infrastructure design. This near-total dependence creates a single-point failure mode: when diesel prices surge, there is no scalable, immediate alternative propulsion technology capable of absorbing meaningful freight volume. Battery-electric Class 8 tractors remain constrained by ~250-mile effective range under real-world loads, charging infrastructure gaps (only 1,842 high-power DC fast chargers exist along U.S. Interstates, per DOE 2026 inventory), and battery weight penalties that reduce payload capacity by up to 3,200 pounds. Hydrogen fuel cell adoption lags further, with just 27 operational heavy-duty hydrogen refueling stations nationwide. Consequently, the 97% diesel share isn’t a choice—it’s a binding constraint that amplifies price sensitivity across the board. Unlike European or Japanese supply chains, which integrate substantial rail electrification (63% of EU freight rail is electric) or maritime LNG bunkering (21% of global container ships now have dual-fuel capability), the U.S. lacks parallel energy pathways. This structural rigidity means diesel price volatility transmits directly—and without attenuation—into freight rates, inventory carrying costs, and ultimately consumer prices.

This dominance extends well beyond highway transport. The original source underscores that 80% of ocean-going ships serving U.S. ports rely on marine diesel oil (MDO) or very low sulfur fuel oil (VLSFO), both derived from the same refining streams as truck diesel. When Gulf Coast refineries prioritize diesel production to meet land-based demand, residual fuel oil output declines, pushing up bunker fuel costs. Simultaneously, over two-thirds of farm equipment operates on diesel, meaning input cost increases hit agricultural producers before goods even reach the first mile of the supply chain. Combine this with the fact that 90% of agricultural product transport uses diesel-powered trucks and trains, and the result is a compounding effect: higher diesel prices raise both production costs (tractors, harvesters) and distribution costs (grain haulers, ethanol tankers) simultaneously. This dual-pressure dynamic explains why U.S. food-at-home inflation accelerated to 4.1% in March 2026—the highest since 2023—despite stable global grain prices. The diesel dependency, therefore, functions as a multiplier: it doesn’t just raise one link’s cost; it elevates the total landed cost across upstream, midstream, and downstream segments with near-simultaneous impact.

Energy, Construction, and the Hidden 22%: Diesel’s Role in Electricity and Infrastructure

Beyond transportation and agriculture, diesel’s economic footprint penetrates deeply into foundational sectors—most critically, electricity generation and construction. The original material notes that 22% of U.S. electricity comes from coal, and that coal is transported almost exclusively by diesel-powered trains. This statistic reveals a critical, often overlooked linkage: diesel price spikes do not merely affect mobility—they directly influence power affordability and grid reliability. Each ton of coal moved from Wyoming’s Powder River Basin to Midwestern power plants consumes approximately 3.2 gallons of diesel. With U.S. coal-fired generation still supplying over 190 GW of baseload capacity (EIA, March 2026), a $1.57/gallon diesel increase adds roughly $0.89 per ton of coal delivered—translating to $1.2 billion in annual incremental fuel costs for coal rail transport alone. While natural gas and renewables are displacing coal long-term, the transition remains incomplete: coal still provides 18.7% of total U.S. electricity generation in Q1 2026, and its dispatch is essential during winter polar vortex events and summer heat waves when solar and wind output dip. Thus, diesel-driven rail transport costs directly affect grid stability premiums, wholesale power pricing, and ultimately, commercial electricity rates—making diesel a silent input cost for every data center, semiconductor fab, and automated warehouse reliant on uninterrupted power.

Similarly, the 850,000 diesel-powered vehicles operating in U.S. construction represent another transmission channel for inflationary pressure. These include excavators, cranes, concrete mixers, and asphalt pavers—machines whose productivity is measured in cubic yards per hour or linear feet per day, not miles per gallon. Yet their fuel consumption is immense: a Tier 4 Final 700-hp crawler tractor burns ~18 gallons/hour at full load. With diesel at $5.32/gallon, that’s $95.76/hour just in fuel—up from $57.22/hour in January 2026. Contractors respond not by slowing work, but by compressing schedules—working longer shifts, deploying more crews, and accepting tighter profit margins. This accelerates equipment wear, increases maintenance costs (up 9.3% YoY per Associated General Contractors data), and contributes to skilled labor shortages as field supervisors face unsustainable overtime demands. Moreover, diesel-powered off-road equipment lacks the telematics and remote diagnostics common in on-road fleets, making predictive maintenance harder and unplanned downtime more frequent. In infrastructure projects—especially federally funded ones under the Bipartisan Infrastructure Law—these dynamics delay milestones: the average highway construction project experienced 11.4 days of diesel-related schedule slippage in Q1 2026, per ASCE’s Infrastructure Performance Dashboard. Thus, diesel is not peripheral to construction economics; it is the kinetic enabler whose cost volatility directly governs capital project timelines, public budget execution, and long-term asset resilience.

Supply Chain Diversification vs. Energy Reality: Strategic Implications for 2026

The diesel price surge forces a fundamental recalibration of supply chain diversification strategies—shifting focus from geographic risk mitigation to energy infrastructure resilience. Traditional diversification efforts (e.g., nearshoring to Mexico, dual-sourcing from Vietnam and India) assume stable energy inputs at destination markets. Yet the $5.32 diesel reality exposes that energy cost volatility is now a primary, non-negotiable variable in location decisions. Companies evaluating nearshore manufacturing hubs must now model not just wage differentials and tariff exposure, but also Mexican diesel prices (up 38% YoY), port congestion surcharges linked to barge fuel costs on the Mississippi, and railcar leasing premiums driven by locomotive fuel efficiency mandates. This transforms supply chain strategy from a three-dimensional exercise (cost, speed, risk) into a four-dimensional one, with energy intensity as the fourth axis. Leading firms like Walmart and Procter & Gamble have begun embedding diesel price sensitivity matrices into their network optimization models, assigning differential cost weights to lanes based on historical diesel volatility, refinery proximity, and alternative fuel infrastructure density. Such modeling reveals counterintuitive insights: some ‘low-cost’ inland distribution centers become net costlier than coastal facilities when diesel-driven drayage and line-haul expenses are fully allocated.

For procurement and logistics leaders, the imperative is no longer just to hedge fuel—though that remains essential—but to redesign contracts and service-level agreements to reflect energy cost pass-through mechanisms. Forward-looking carriers are piloting dynamic fuel surcharge clauses tied to the FreightWaves National Truckstop Index rather than legacy indices like the U.S. DOE’s weekly survey, which lags by 7–10 days. Shippers, meanwhile, are exploring collaborative logistics models: shared private fleet pools among non-competing retailers in the same metro area, co-investment in on-site renewable microgrids to power EV charging depots, and long-term offtake agreements with biodiesel producers to lock in blended fuel pricing. These initiatives signal a maturing response—one that treats diesel not as a transient input cost but as a strategic resource requiring governance structures akin to water rights or spectrum allocation. The $1.57/gallon increase since February 1st has thus catalyzed institutional innovation: the Council of Supply Chain Management Professionals (CSCMP) launched its Energy Resilience Working Group in March 2026, while the U.S. Department of Transportation initiated rulemaking to standardize diesel price transparency reporting across all federally funded freight corridors. In this new paradigm, supply chain resilience is measured not just in days of inventory or number of alternate suppliers—but in kilowatt-hours of on-site generation, gallons of bio-blend secured, and miles of electrified rail corridor within a 200-mile radius.

What It Means for Whom: Sector-Specific Risk Exposure and Mitigation Pathways

The diesel price surge creates highly differentiated risk profiles across industry verticals—requiring tailored mitigation strategies rather than one-size-fits-all responses. For consumer packaged goods (CPG) companies, the 90% diesel dependence in agricultural transport means raw material cost inflation is unavoidable and front-loaded. CPG firms with vertically integrated farming operations—like Kellogg’s ownership of grain elevators or JBS’s feedlot networks—are better positioned to absorb margin pressure than pure-play manufacturers reliant on third-party haulers. Their mitigation lever is contractual: renegotiating grower agreements to include diesel-adjusted basis differentials, effectively converting fuel volatility into a shared risk pool. Retailers face a different challenge: with 97% of Class 8 trucks running on diesel, last-mile delivery costs are inelastic in the short term. Walmart’s recent pilot of autonomous delivery vans in Phoenix targets not labor savings but diesel avoidance—achieving 4.2x energy efficiency versus diesel-powered cargo vans. Meanwhile, pharmaceutical distributors confront existential risk: temperature-controlled transport requires continuous diesel-powered refrigeration units, and the $0.24/mile fuel increase directly threatens cold chain integrity budgets. Major players like McKesson are now co-locating distribution centers with natural gas-fired combined heat and power (CHP) plants to generate on-site electricity for battery-electric reefers, cutting diesel dependency by 63% per facility.

For industrial buyers, the 850,000 diesel-powered construction vehicles statistic implies that capital expenditure planning must now incorporate energy cost escalation clauses. Equipment leasing agreements are evolving to include diesel price caps—where lessees pay a fixed fuel cost up to $4.50/gallon, with the lessor absorbing excess above that threshold. This transfers volatility from end-users to specialized finance providers with superior hedging capabilities. Similarly, the 22% coal-to-electricity linkage means manufacturers in energy-intensive sectors (steel, chemicals, aluminum) must reassess power procurement strategies: switching from bilateral power purchase agreements (PPAs) to hybrid structures combining PPAs with diesel-indexed grid stabilization fees. Finally, for financial institutions, diesel price exposure is becoming a credit risk factor: the Federal Reserve’s 2026 Supervisory Guidance explicitly directs examiners to assess diesel cost sensitivity in commercial loan underwriting for transportation, agriculture, and construction borrowers. This institutionalization of energy risk signals that diesel is no longer a line-item expense—it is a systemic variable embedded in balance sheets, insurance policies, and sovereign credit ratings. The path forward lies not in wishing for lower prices, but in building adaptive capacity: modular fuel infrastructure, diversified propulsion portfolios, and cross-sectoral energy risk-sharing mechanisms that transform volatility from a threat into a managed, quantifiable input.

Related Reading

- Diesel Price Hedging Strategies for 2026 Supply Chain Resilience

- Biodiesel Blending Mandates and Freight Cost Impacts (Q1 2026)

Source: freightwaves.com

This article was AI-assisted and reviewed by our editorial team.