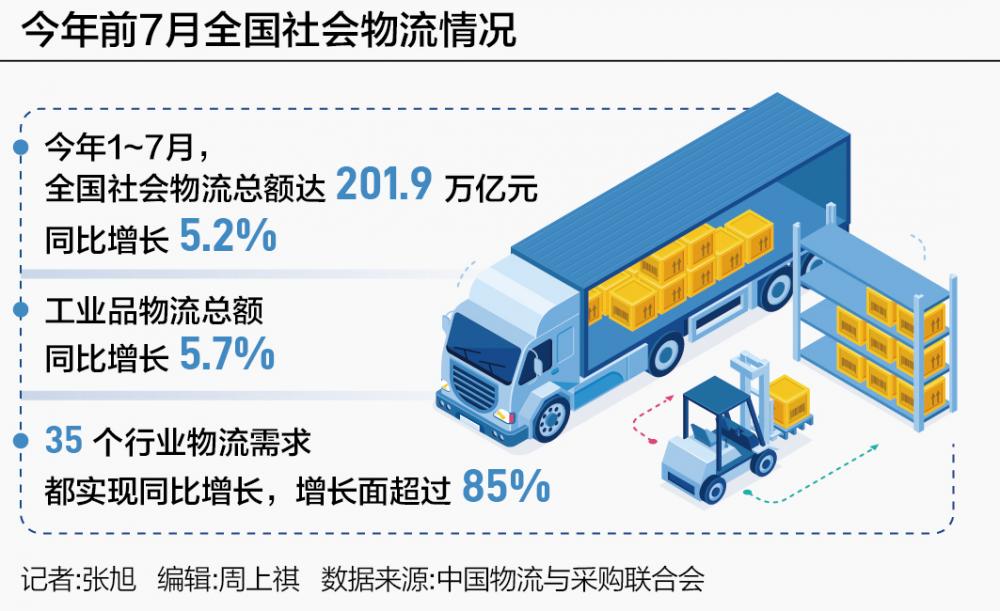

China’s logistics sector has crossed a historic threshold—reaching $20.19 trillion in total social logistics value in the first seven months of 2025, according to data released by the China Federation of Logistics & Purchasing (CFLP). This represents a 5.2% year-on-year growth, with industrial logistics—the movement of raw materials, components, and finished goods across manufacturing supply chains—accounting for over 82% of the total. Notably, high-end manufacturing logistics alone grew 9.3% YoY in July 2025, outpacing overall industrial freight growth by 0.5 percentage points. These figures are not merely macroeconomic indicators; they signal a structural realignment in China’s supply chain architecture—one where logistics is no longer a cost center but the central nervous system enabling advanced industrial transformation.

The Industrial Anchor: Why Manufacturing Logistics Now Drives National Resilience

For decades, China’s logistics narrative was dominated by e-commerce parcel volumes and last-mile delivery efficiency. Today, that paradigm has decisively shifted. Industrial logistics now constitutes the overwhelming majority of freight tonnage, value, and strategic investment. The CFLP data reveals that industrial goods logistics rose 5.7% YoY from January to July 2025—outpacing both consumer logistics and agricultural logistics—and all 35 tracked industries reported positive YoY growth, with an expansion breadth exceeding 85%. This near-universal growth signals systemic health: it reflects sustained production demand, robust capital expenditure cycles, and deepening integration across upstream and downstream nodes.

Crucially, this isn’t just volume growth—it’s value-driven sophistication. As Lin Dan, Chief Researcher at the China Academy of Transport Sciences and Director of the Transport Industry & Logistics Center, explained to 21st Century Business Herald, the stability and resilience of China’s industrial logistics reflect the underlying strength of its manufacturing base: “Industrial logistics demand remains steadily expanding—a clear sign that China’s industrial economy retains strong fundamentals, production demand continues to grow, and macroeconomic momentum remains solid.” Lin’s assessment is corroborated by inventory turnover metrics, factory utilization rates, and procurement manager indices (PMIs), all of which have remained above the 50-point expansion threshold for eight consecutive months.

This industrial anchor serves three critical functions: First, it buffers external volatility—when global trade slows or tariffs rise, domestic industrial circulation absorbs shock. Second, it enables scale-driven innovation—large-volume, high-frequency logistics flows generate rich operational data essential for AI model training and optimization. Third, it creates gravitational pull for infrastructure investment: over 72% of new smart warehouse deployments in 2024–2025 were commissioned by Tier-1 automotive, semiconductor, and medical device manufacturers—not retailers.

AI+Advanced Manufacturing: The New Logistics Growth Engine

The most consequential trend emerging from the $20 trillion logistics surge is the rapid convergence of artificial intelligence and high-end manufacturing logistics. Policy frameworks like the State Council’s August 2025 Guiding Opinions on Deepening the ‘AI+’ Initiative and the Ministry of Transport’s newly approved Implementation Guidelines for ‘AI+ Transportation & Logistics’ formalize what industry practitioners have already experienced: logistics is becoming the primary vector through which AI permeates industrial operations.

Consider the growth differentials: In July 2025, logistics demand for high-tech manufacturing surged 9.3% YoY. Within that category, specific segments showed explosive acceleration:

- Semiconductor equipment & simulation chips: +23.1% YoY logistics volume

- Industrial control computers & embedded systems: +21.7% YoY

- 3D printing hardware & precision tooling: +20.4% YoY

- EV battery cells & cathode/anode materials: +22.6% YoY

- Medical robotics & diagnostic imaging subsystems: +19.8% YoY

These aren’t isolated spikes—they reflect coordinated investment in intelligent factories. IDC reports that the share of Chinese industrial enterprises deploying large language models (LLMs) and multimodal AI agents in logistics planning rose from 9.6% in 2024 to 47.5% in 2025. More significantly, China hosts 85 of the world’s 189 officially designated ‘Lighthouse Factories’—a figure representing 45% of the global total—and over 92% of these facilities run integrated AI-powered logistics orchestration platforms that dynamically optimize inbound material sequencing, AGV routing, cross-dock scheduling, and predictive maintenance logistics.

This shift redefines logistics KPIs. Traditional metrics like on-time-in-full (OTIF) are being augmented—or replaced—by AI-specific indicators: model inference latency per shipment decision, real-time constraint satisfaction rate, and logistics carbon intensity per AI-optimized route. The result is a virtuous cycle: smarter logistics enable faster product iteration, which fuels more complex supply chains, which in turn demand even more sophisticated logistics intelligence.

Regional Rebalancing: The Rise of the West-Central Logistics Corridor

Geographically, the $20 trillion logistics wave is reshaping China’s economic map. Historically concentrated in coastal export hubs, logistics activity is now rapidly decentralizing. July 2025 regional business volume indices reveal a decisive pivot: the Western region posted a 52.3 index, 1.8 points above the national average; the Central region scored 50.9, 0.4 points above average; while the Eastern region held steady at 50.3. This is not statistical noise—it reflects deliberate state-backed infrastructure deployment, policy incentives, and industrial relocation.

Key drivers include:

- The completion of the Chengdu-Chongqing Dual-City Economic Circle logistics backbone, integrating 12 automated inland ports and 3 AI-optimized dry ports;

- The Gansu-Xinjiang New Energy Equipment Corridor, handling >80% of China’s wind turbine blade and solar tracker logistics, with AI-predictive rail slot allocation reducing transit time by 37%;

- The Guangxi-Beibu Gulf Intelligent Manufacturing Hub, where customs clearance AI agents reduced cross-border logistics dwell time from 42 hours to under 9 hours for EV component shipments to ASEAN markets.

This regional rebalancing carries profound implications for global supply chain strategy. Multinationals can no longer treat China as a monolithic manufacturing base. Instead, they must design tiered logistics architectures: high-speed air-rail networks linking Chengdu and Xi’an to global tech hubs for R&D-critical components; heavy-haul green corridors from Ningxia to Shanghai for bulk battery materials; and localized micro-fulfillment ecosystems around Wuhan and Zhengzhou for electronics assembly logistics. The era of ‘one-China-logistics-strategy’ is over—replaced by a multi-layered, AI-governed, regionally specialized logistics topology.

From Infrastructure to Intelligence: The ‘1+N+X’ Logistics Operating System

Underpinning this transformation is China’s institutional leap from physical infrastructure development to intelligent operating system construction. The Ministry of Transport is rolling out the ‘1+N+X’ Integrated Transport & Logistics Large Model Framework—a foundational architecture designed to unify logistics intelligence across sectors. As officials clarify, the framework consists of:

- ‘1’ Unified Foundation Model: A nationally hosted, open-weight LLM trained exclusively on 200+ million anonymized logistics documents—including bills of lading, customs declarations, equipment telemetry, and port congestion logs;

- ‘N’ Vertical Domain Models: Specialized fine-tuned variants for aviation cargo, rail intermodal, cold chain pharma, hazardous materials, and cross-border e-commerce logistics;

- ‘X’ Enterprise-Specific Applications: Plug-and-play AI modules for dynamic lane pricing, autonomous yard management, predictive customs risk scoring, and multimodal carbon accounting.

This is not theoretical. Pilots in Shenzhen’s Yantian Port and Tianjin’s Binhai New Area have already demonstrated 28% reduction in container dwell time, 19% improvement in berth utilization, and 33% faster customs release for AI-verified shipments. Crucially, the framework is interoperable with private-sector platforms—Alibaba’s Cainiao, JD Logistics, and SF Express all contribute proprietary logistics data under strict data sovereignty protocols, enriching the national model without compromising competitive advantage.

The ‘1+N+X’ system transforms logistics from a fragmented service layer into a coherent, self-optimizing infrastructure layer—akin to how 5G became the connectivity substrate for IoT. For global shippers, this means standardized AI interfaces, predictable regulatory logic, and machine-readable policy compliance—all accessible via API. It also means that logistics intelligence is becoming a public good, lowering the barrier to entry for SME manufacturers seeking AI-powered supply chain agility.

Strategic Implications for Global Supply Chains

What does China’s $20 trillion logistics evolution mean for international stakeholders? Three imperatives emerge:

First, supply chain mapping must evolve beyond Tier-1 suppliers to include logistics intelligence partners. A Tier-1 auto supplier in Changsha may be technically sound—but if its logistics partner lacks API access to the national rail AI scheduler or cannot integrate with the Guangdong EV Battery Logistics Consortium’s predictive inventory model, it becomes a systemic bottleneck. Due diligence now requires evaluating logistics AI readiness alongside technical certifications.

Second, geopolitical risk modeling must incorporate logistics AI maturity. Countries with nascent logistics AI ecosystems face higher exposure to disruptions—from port congestion cascades to customs delays triggered by manual document review. Conversely, nations leveraging China’s logistics AI infrastructure (e.g., via ASEAN-China rail corridors) gain resilience through algorithmic predictability—even amid tariff volatility.

Third, the definition of ‘nearshoring’ is being redefined. Nearshoring is no longer just about geography—it’s about logistics proximity to intelligence. A German automaker sourcing batteries from Sichuan may be ‘farther’ geographically than one sourcing from Poland, but with AI-optimized air-rail-barge multimodal routing and real-time customs pre-clearance, its end-to-end lead time is 22% shorter and 41% more predictable. Logistics intelligence is becoming the new geography.

In conclusion, China’s $20 trillion logistics surge is not a story about trucks and warehouses. It is the visible manifestation of a deeper industrial metamorphosis—one where logistics, powered by AI and anchored in advanced manufacturing, has become the principal engine of economic upgrading, regional rebalancing, and technological sovereignty. For global supply chain leaders, understanding this shift is no longer optional. It is the prerequisite for competitiveness in the next decade.

Source: ‘200 Trillion Logistics Surge: Industrial Share Exceeds 80%, AI+Advanced Manufacturing as Core Engine’, 21st Century Business Herald, September 9, 2025.