The Charcoal on That Truck Costs More to Import, More to Buy, and Is Headed to a Cookout That Runs 13% Higher Than Last Year. Here Is What That Tells You About the Consumer Right Now.

The Import Shipment Data

Start with what the trade data actually shows.

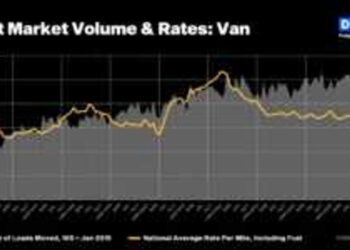

According to Volza’s charcoal briquette import tracking, U.S. buyers imported 403 shipments of charcoal briquettes in the twelve months ending May 2025 — a 95% increase compared to the prior twelve-month period. That near-doubling of import shipment count reflects two things happening simultaneously: genuine demand recovery as the post-pandemic grilling market normalized, and front-loading behavior as importers anticipated tariff escalation and pulled inventory forward before new duties locked in. Indonesia, Paraguay, and Singapore were the top three source countries for those shipments.

- Global wood charcoal exports reached $1.53 billion in 2024 according to ITC Trade Map data — up 16% from $1.32 billion in 2020, but down 3.9% from the 2023 peak of $1.59 billion.

- The five largest exporters by revenue in 2024 were Indonesia, Laos, Vietnam, the Philippines, and mainland China, which together captured 46.4% of global charcoal export revenues.

- The United States sits in the second tier of global importers by value, alongside Saudi Arabia, Germany, and the UK — with the first tier dominated by China, Japan, and South Korea absorbing the highest dollar values.

The average import price for charcoal fell to $526 per ton in 2024 — a meaningful correction from the elevated price levels of 2022 and 2023, when supply chain disruptions and logistical cost spikes pushed import prices to their recent highs. That price correction is what enabled the 95% surge in import shipment volumes: lower per-unit cost made volume purchases more attractive for U.S. importers building inventory ahead of the 2025 and 2026 grilling seasons.

The Tariff Disruption That Is Already in the Supply Chain

Here is where the 2026 picture moves sharply from 2024 and 2025, and also where the freight implications become specific.

Indonesia is the dominant global charcoal exporter and one of the primary sources of the premium lump charcoal that has grown in market share at U.S. retail. In April 2025, the Trump administration imposed a 32% import tariff on Indonesian goods as part of the reciprocal tariff package which is up from prior rates that ranged from 0% to 5% depending on product category. That tariff did not immediately end Indonesian charcoal imports to the U.S., but it materially increased their landed cost and created sourcing uncertainty that has driven U.S. importers to evaluate alternative suppliers.

The U.S.-China tariff situation adds another layer. Charcoal imports from China, which supplies both finished product and production inputs, fell into the disrupted trade pattern that saw U.S. imports from China trend 27% lower year-to-date through late 2025 compared to 2024, with some months running 40% below prior-year volumes. For charcoal specifically, the Chinese export to U.S. is a smaller component of total supply than Indonesian or Paraguayan product, but the disruption in China-sourced supply created additional pressure on the alternative supply chains that were already absorbing the Indonesian tariff impact.

Paraguay, the second major source country for U.S. charcoal imports, faces its own trade complications. Paraguayan charcoal exports are heavily weighted toward hardwood lump product favored by the premium BBQ market, and the country’s export capacity has been shaped by deforestation regulations and bilateral trade agreements that do not include the same tariff buffers that larger trading partners negotiated. Import costs on Paraguayan charcoal have risen with the broader tariff and logistics cost environment, contributing to the per-unit price increase that retailers are managing at the shelf level.

The bottom line for the freight that moved this spring: U.S. charcoal importers front-loaded heavily through early 2025, anticipating that tariff escalation would make summer purchasing more expensive. That front-loading generated the 95% shipment volume surge in the trailing twelve months ending May 2025, and it means that the charcoal sitting on retailer shelves this Memorial Day weekend largely arrived months ago, before the most aggressive tariff rates took effect. What arrives for the Fourth of July and Labor Day seasons will cost more at the import level if supply chains have not been restructured in the interim.

What the Consumer Sees at the Store

The import data describes one end of the supply chain. The retail price data describes what landed when the chain is complete, and the 2026 picture at the consumer level is significantly more expensive than the 2024 baseline.

Barbecue staples like burgers, hot dogs, watermelon, and core cookout goods, are up an average of 13% in 2026 compared to last year, according to a Groundwork Collaborative and Century Foundation analysis published this week. Six ears of yellow corn average $5.90 today versus $2.97 last year which is a 98% increase driven by weather-related production disruptions and commodity cost pressures that have nothing to do with charcoal but everything to do with the household budget available for the cookout.

The beef numbers are the most acute pressure point. USDA Economic Research Service data shows all-fresh beef averaged a record $9.64 per pound nationally in April 2026 which is up $1.14 per pound, roughly 13%, from April 2025. Ground chuck hit $6 per pound, up 14% year over year. The driver is structural: the U.S. cattle herd is at its smallest level since 1961, a 74-year low produced by years of drought that forced herd liquidation faster than ranchers could rebuild. Rabobank’s Senior Beef Analyst Lance Zimmerman noted that demand for beef is expected to reach a 39-year high in 2026 even as supply contracts, a dynamic that keeps prices elevated regardless of what happens to tariffs on the import side.

Rabobank’s BBQ Index puts the current cost of a Memorial Day cookout for ten people, one cheeseburger and one chicken sandwich each, at approximately $103, up from $73 in 2018. The cumulative seven-year increase in cookout cost is not primarily a tariff story. Over 90% of U.S. barbecue ingredients are domestic. It is an input cost, supply constraint, and logistics cost story that has been building across the entire food supply chain and it is now visible on every receipt at every grocery checkout between here and Memorial Day.

The Kingsford Earnings Timeline: The Closest Thing to a Real-Time Grilling Gauge

Kingsford holds the dominant share of the U.S. charcoal briquette market by a significant margin which means Clorox’s quarterly earnings reports are as close to a real-time read on American grilling behavior as any public data source provides. The arc of those results across the past four reporting periods tells a specific and consistent story.

Clorox’s fiscal year runs July through June, which means Q4 (the quarter ending June 30) captures the peak of grilling season including Memorial Day and the Fourth of July. That quarter historically generates roughly 50% of annual Kingsford revenue. It is the most important data point in the brand’s calendar.

In Q3 fiscal year 2025 (the quarter ending March 2025), Clorox reported that the Household segment, which includes Kingsford under Bags and Wraps, Cat Litter, and Grilling also saw net sales decrease 11%, driven by 9 points of lower volume and 2 points of unfavorable price mix. The specific call-out in the earnings release: lower Kingsford volume was driven by lower consumption, a timing shift in Kingsford shipments, and retailer promotional timing adjustments. That is a company describing a demand environment where consumers are grilling less frequently than the prior year and retailers are being cautious about inventory builds heading into the peak season.

Q4 fiscal year 2025, the quarter that captures Memorial Day 2025, told a more complicated story. Net sales for the full Clorox company increased 4%, but Clorox’s CFO flagged that approximately 13 to 14 points of that benefit came from incremental ERP transition-related shipments which is a one-time inventory build ahead of a new enterprise software system not from underlying consumer demand (important to note if you are tracking the data). On the Kingsford side specifically, the Q4 2025 earnings call produced one of the most candid public statements about the brand’s Memorial Day performance in recent memory. Clorox CEO Linda Rendle said directly:

“I think you all know there was some pretty terrible weather in Q4 for Memorial Day. Frankly, it came down to us not executing to the degree we know we can and we must execute on Kingsford in the key holidays. That’s what happened in Memorial Day. We had slightly less merchandising and not necessarily on the right sizes as we shifted our plan.”

She added that consumers are increasingly requesting smaller sizes — buyers who want charcoal for one or two grilling occasions rather than the large twin-pack formats that dominated pandemic-era purchasing.

Moving into fiscal year 2026, Q1 (ending September 2025) saw Clorox overall organic sales decline 3% with Kingsford contributing to weakness in the Household segment. Q2 fiscal 2026 (ending December 2025) showed the Household segment down 6%, 3 points from lower volume, 3 points from unfavorable price mix and with the volume decrease attributed specifically to lower consumption. The full fiscal year 2026 outlook Clorox confirmed in February projects net sales down 6% to 10%, partly reflecting the reversal of those ERP-related shipment benefits that inflated the prior year’s numbers.

Read together, these four quarters paint a specific picture for anyone trying to understand what moves through a charcoal distribution network heading into Memorial Day 2026. The domestic consumer charcoal market is operating below its pandemic peak, below its post-cyberattack recovery high, and in a promotional environment where retailers are discounting aggressively to drive volume amid constrained household budgets.

Source: FreightWaves

Compiled from international media by the SCI.AI editorial team.