According to www.aircargonews.net, European airlines and integrators have rapidly expanded air cargo capacity on the Asia-Europe trade lane to offset sharp declines caused by the Middle East conflict — with direct freighter and widebody capacity rising 31% in the week ending 21 March compared to the week ending 28 February, just before hostilities escalated.

Capacity Shifts by Region and Carrier Type

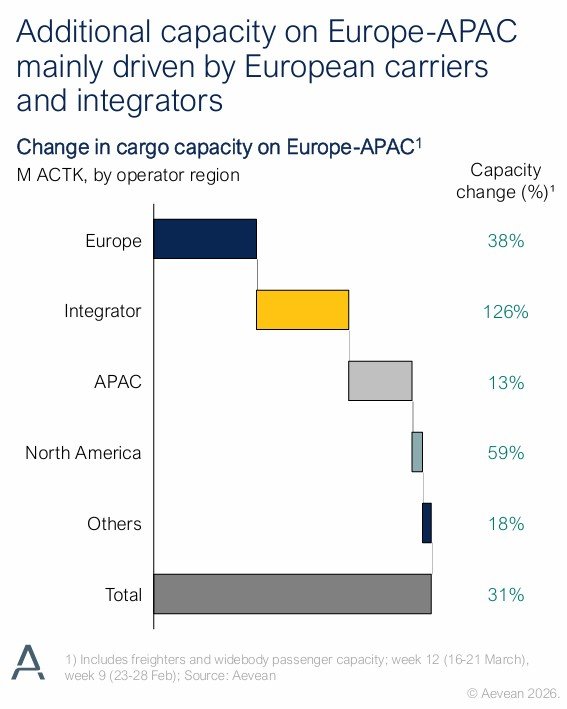

Aevean’s research shows divergent responses across carrier groups:

- European-based airlines increased cargo capacity by 38% week-on-week — the largest absolute tonne-kilometre gain due to their higher baseline;

- Integrators boosted capacity by 126%, though from a smaller starting point;

- Asia Pacific airlines added 13% capacity;

- North American carriers increased space by 59%.

Globally, air cargo capacity was down 2% year on year — a marked improvement from the 20% decline observed at the peak of the crisis last year. Meanwhile, capacity between the Asia Pacific and the Middle East fell 24% year on year, and Middle East–to–Europe routes declined 15%. In contrast, Asia Pacific–to–Europe capacity surged 31%.

Operational Responses from Key Carriers

Uzbekistan-based My Freighter launched new weekly services effective 29 March, linking Hanoi (HAN), Bangkok (BKK), Almaty (ALA), and Tashkent (TAS) with Frankfurt Airport (FRA) via its TAS hub. The airline described the move as part of its broader network expansion plans.

DHL Global Forwarding responded to surging demand by leveraging the DHL Express network: it introduced weekly dedicated flights connecting Shanghai to Leipzig and Liège to Hong Kong. This integration of express and forwarding assets enables faster, more reliable capacity deployment without relying on third-party belly-hold space.

Lufthansa Cargo announced additions to its summer freighter schedule, including extra transpacific services and new capacity to Delhi — reflecting both regional demand shifts and strategic route diversification beyond traditional Middle East corridors.

Industry Context for Supply Chain Professionals

This reallocation mirrors broader industry adaptation to geopolitical volatility. Since late 2023, Red Sea disruptions have already driven rerouting via the Cape of Good Hope, increasing ocean transit times by 10–14 days and amplifying pressure on air cargo for time-sensitive goods. Major integrators like FedEx and UPS previously reported double-digit air freight volume growth on Asia–Europe lanes in Q1 2024, while Maersk’s 2024 Logistics Outlook highlighted that 72% of shippers now prioritize route redundancy over pure cost optimization. For supply chain professionals, these developments underscore the growing operational necessity of multi-airline contracting, dynamic tendering windows, and real-time capacity monitoring — especially for high-value electronics, pharmaceuticals, and automotive components where lead-time variability directly impacts production schedules and inventory carrying costs.

Source: Air Cargo News

Compiled from international media by the SCI.AI editorial team.