According to www.dcvelocity.com, demand for smaller “shallow-bay” warehouse space is rising across U.S. industrial real estate markets, driven by service-oriented users and last-mile distribution needs—even as broader U.S. economic growth slows.

Defining Shallow-Bay Space

CBRE defines shallow-bay properties as industrial buildings under 50,000 square feet with clear heights between 14 and 28 feet. This contrasts sharply with the dominant big-box warehouse developments that have proliferated since 2017. While new supply surged in large-format logistics facilities, shallow-bay construction remained limited—leading to persistent supply constraints.

Supply-Demand Imbalance Deepens

Shallow-bay vacancy began falling below the overall industrial vacancy rate starting in 2017, and the gap widened significantly during the recent development cycle. By early 2024, shallow-bay vacancy was 2.5 percentage points below the national industrial vacancy rate—a clear indicator of tight availability amid sustained leasing activity.

Compounding the scarcity, the existing inventory is overwhelmingly aged:

- Nearly half of shallow-bay inventory was built prior to 1980

- More than 80% was built before 2000

- Properties built since 2010 account for only 5% of total inventory

This aging stock reflects structural barriers to new development—including high land costs and zoning policies in major metropolitan areas that favor larger-scale projects over smaller, service-oriented facilities.

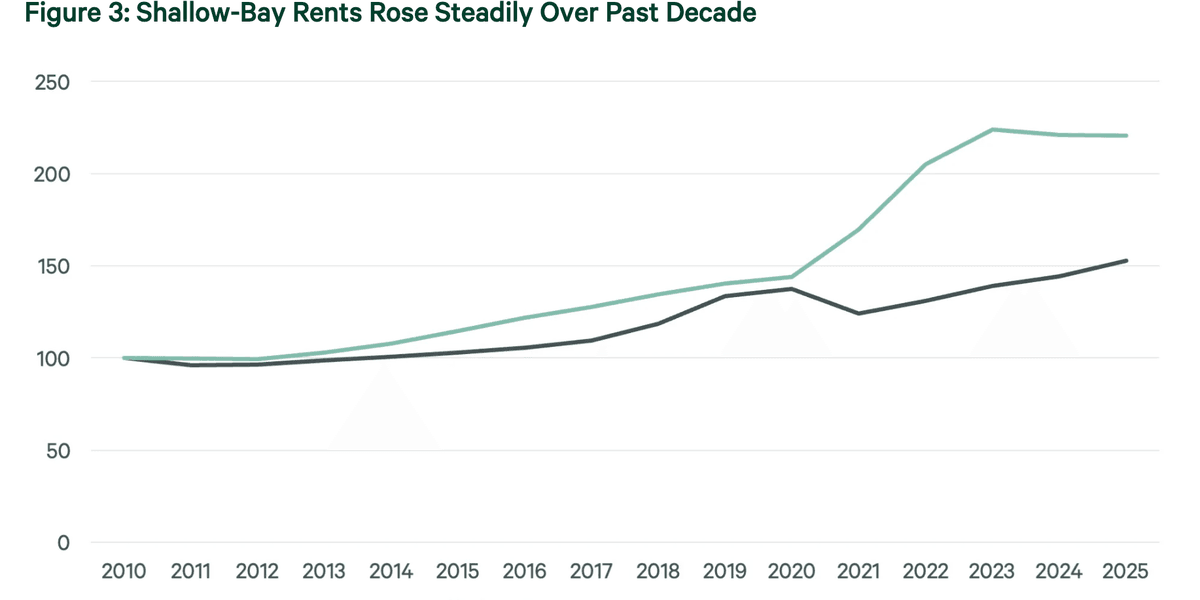

Rent Growth Reflects Enduring Demand

By 2025, shallow-bay asking rents were more than 50% higher than 2010 levels. This durable rent appreciation underscores both consistent demand from small- and mid-sized businesses serving local economies and the chronic lack of new supply.

The trend aligns with broader industry shifts toward decentralized fulfillment networks. As e-commerce logistics evolve beyond centralized mega-distribution centers, demand has grown for flexible, geographically dispersed facilities capable of supporting rapid local delivery—especially in dense urban and suburban corridors where shallow-bay properties are often located.

This dynamic mirrors parallel developments elsewhere: DHL recently announced a significant expansion of its North America data center logistics (DCL) infrastructure, launching 10 dedicated warehouse sites totaling more than seven million square feet in 2026—many of which will support specialized, high-touch, localized deployment workflows. Similarly, Arvato’s 270,000-square-foot expansion in Denton, Texas, emphasizes secure, white-glove handling and last-mile coordination for AI data center hardware—functions well-suited to smaller, adaptable facilities rather than monolithic warehouses.

For supply chain professionals, this means procurement and network design strategies must now explicitly account for shallow-bay capacity—not just as fallback options, but as core nodes in resilient, responsive fulfillment architectures. Lease negotiations require deeper due diligence on building age, ceiling height compatibility with automation, loading dock configuration, and proximity to municipal road networks—not just square footage and base rent. Moreover, with new construction unlikely to meaningfully increase supply in the near term, forward-looking teams are prioritizing retrofit feasibility, modular automation integration, and multi-tenant co-location models to maximize utility from constrained older assets.

Source: DC Velocity

Compiled from international media by the SCI.AI editorial team.