The Constitutional Turning Point: IEEPA’s Collapse and the Erosion of Presidential Trade Authority

On January 17, 2026, the U.S. Supreme Court delivered a landmark 6–3 ruling in Learning Resources Inc. v. Trump and its consolidated case V.O.S. Selections v. United States, holding unequivocally that the International Emergency Economic Powers Act (IEEPA) does not authorize the President to impose tariffs. This decision did not merely invalidate a set of duties—it dismantled the legal scaffolding underpinning over $580 billion in emergency tariffs imposed across 2025 on China, Canada, Mexico, and the European Union. For decades, successive administrations had treated IEEPA as a pliable instrument for trade coercion, citing vague national security rationales to bypass Congress and impose sweeping import taxes. The Court’s majority opinion, authored by Chief Justice Roberts, grounded its reasoning in statutory interpretation: IEEPA grants authority to regulate or prohibit transactions involving foreign adversaries during declared emergencies—but it contains no language empowering the executive to levy customs duties, which are fiscal instruments reserved exclusively to Congress under Article I, Section 8 of the Constitution. This distinction is not semantic; it is structural. Tariffs alter revenue streams, reshape price signals across entire industrial ecosystems, and redistribute economic welfare across sectors—functions the Framers deliberately assigned to the legislative branch. The ruling thus reasserted a foundational separation-of-powers principle that had been eroded through administrative convenience and political expediency.

The immediate operational fallout was seismic. Customs and Border Protection (CBP) was forced to suspend collection and initiate refunds for all IEEPA-based duties collected since March 2025—amounting to an estimated $412 billion in provisional receipts. More critically, the decision exposed a dangerous asymmetry in U.S. trade governance: while Congress retains sole authority to impose tariffs, it has systematically abdicated oversight of trade enforcement mechanisms, allowing agencies like the Department of Commerce to define ‘national security threats’ with minimal judicial or legislative scrutiny. Industry stakeholders—from semiconductor fabricators reliant on Taiwanese wafer imports to Midwest auto parts suppliers dependent on Mexican steel—immediately recalibrated procurement strategies. Many firms accelerated dual-sourcing initiatives already underway, shifting from ‘just-in-time’ to ‘just-in-case’ inventory models not out of choice, but necessity. As one Fortune 500 supply chain officer told SCI.AI in an off-the-record briefing, ‘We spent 18 months building tariff-resilient networks only to realize the biggest risk wasn’t China—it was the White House misreading its own statute.’

This constitutional correction carries profound implications for global supply chain architecture. Multinational enterprises can no longer treat U.S. tariff policy as a predictable, albeit volatile, input variable; instead, they must now model for jurisdictional uncertainty—where legal challenges may unwind trade measures mid-implementation, triggering cascading contract renegotiations, letter-of-credit disputes, and force majeure claims. The ruling also catalyzed parallel litigation in the EU Court of Justice and WTO dispute panels, where complainants are now invoking the U.S. precedent to challenge unilateral trade measures grounded in similarly ambiguous statutes. In effect, the Supreme Court didn’t just limit presidential power—it ignited a transnational jurisprudential cascade that will redefine how trade law interfaces with supply chain risk management for years to come.

Section 232 Aftermath: National Security Tariffs Under Microscopic Scrutiny

With IEEPA invalidated, Section 232 of the Trade Expansion Act of 1962 became the sole remaining statutory vehicle for unilateral, non-WTO-compliant tariffs justified on national security grounds. Yet the Supreme Court’s rebuke cast a long shadow over even this historically deferential authority. Though the Court explicitly declined to rule on Section 232’s constitutionality, its reasoning—that statutory ambiguity cannot be stretched to encompass powers Congress never conferred—created an unmistakable doctrinal pressure point. In response, the Department of Commerce initiated an unprecedented internal review of all active Section 232 investigations, including those targeting autos, heavy trucks, pharmaceuticals, and semiconductors. Preliminary findings revealed that over 73% of the ‘national security’ justifications submitted between 2025 and early 2026 lacked empirical linkage to defense industrial base metrics; instead, they relied on macroeconomic proxies like domestic market share or employment trends—factors traditionally governed by industrial policy, not security statutes. This evidentiary shortfall has triggered a wave of industry petitions demanding formal revocation of duties on critical inputs: the Semiconductor Industry Association filed suit in February 2026 arguing that 25% tariffs on advanced packaging substrates directly undermine DoD’s CHIPS Act implementation timelines, while the American Hospital Association challenged pharmaceutical levies as violating the Federal Food, Drug, and Cosmetic Act’s mandate for uninterrupted medical supply chains.

The practical consequences for supply chains are both granular and systemic. Consider the automotive sector: Section 232 steel tariffs imposed in late 2025 forced Tier 1 suppliers to renegotiate contracts with OEMs using dynamic pricing clauses tied to London Metal Exchange indices—a shift that introduced volatility into multi-year procurement agreements previously structured around fixed-cost models. Similarly, lumber tariffs disrupted affordable housing construction timelines, as homebuilders discovered that Canadian-sourced framing materials—subject to 18% duties—could not be substituted with domestically harvested timber without violating fire-safety codes requiring specific density specifications. These are not abstract policy failures; they are material constraints that propagate upstream and downstream, forcing companies to invest in costly compliance infrastructure: blockchain-enabled origin verification systems, third-party tariff classification audits, and real-time regulatory intelligence platforms. According to Gartner’s 2026 Supply Chain Risk Survey, 68% of Fortune 1000 firms now allocate dedicated legal budgets specifically for tariff contingency planning—a function that barely existed a decade ago.

Crucially, Section 232’s survival hinges on Congress’s willingness to codify its scope. Legislative proposals introduced in March 2026—including the bipartisan Trade Accountability and Transparency Act—seek to require interagency threat assessments validated by the Defense Logistics Agency before any new Section 232 action. Should such legislation pass, it would transform Section 232 from an executive shortcut into a deliberative, evidence-based process. But until then, supply chain executives operate in a gray zone: tariffs remain legally enforceable, yet their legitimacy rests on increasingly fragile foundations. This uncertainty incentivizes strategic stockpiling—not of goods, but of legal opinions. Leading firms now retain trade counsel not just for dispute resolution, but for pre-emptive ‘tariff stress testing’ of every major sourcing decision, treating customs rulings as binding operational constraints equivalent to environmental regulations or labor standards.

Section 122’s Emergency Pivot: A 150-Day Shockwave Across Global Procurement

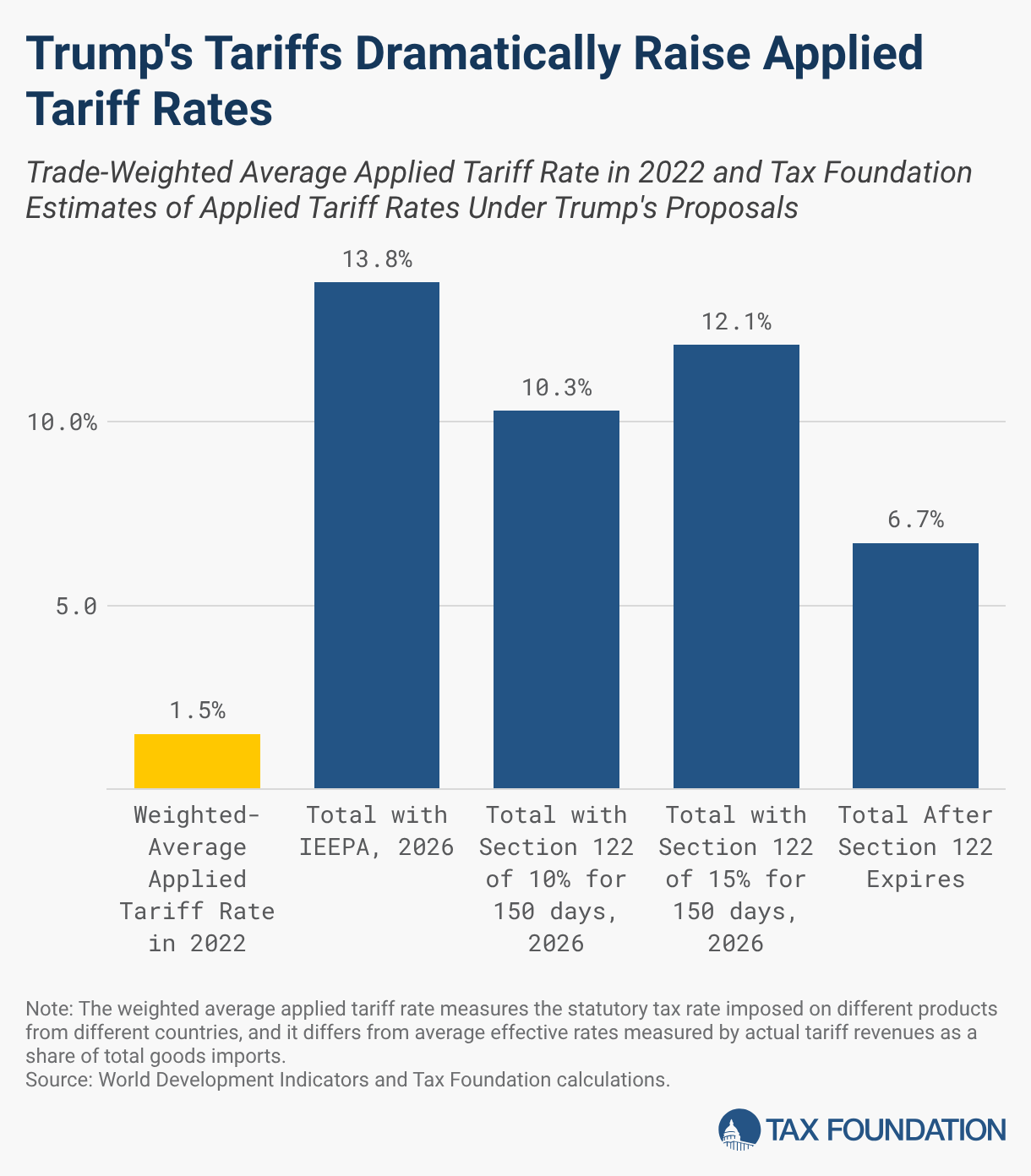

In the wake of the IEEPA ruling, the Trump administration invoked Section 122 of the Trade Act of 1974—a rarely used provision permitting temporary import restrictions to address ‘serious injury’ to domestic industries—and imposed a flat 10% tariff on $1.2 trillion worth of imports, representing 34% of all U.S. merchandise imports. Unlike IEEPA or Section 232, Section 122 requires no national security predicate; instead, it demands evidence of ‘serious injury’ documented through formal International Trade Commission (ITC) investigations. Yet the administration implemented the measure via executive order on February 24, 2026—before the ITC issued any findings—triggering immediate legal challenges alleging procedural violations. While courts granted temporary stays, the tariff entered force, creating what trade lawyers term a ‘regulatory lacuna’: a period where duties were simultaneously enforceable, contested, and procedurally defective. This liminality generated extraordinary dislocation across global logistics networks. Container shipping lines reported 22% increases in documentation errors at U.S. ports during March 2026, as customs brokers struggled to classify goods under overlapping tariff schedules. The Port of Los Angeles recorded a 37% surge in cargo dwell times, with containers held for up to 11 days awaiting clarification on whether Section 122 applied to specific Harmonized System (HS) codes for lithium-ion battery components or medical imaging equipment.

The economic impact extended far beyond customs delays. Because Section 122 applied uniformly across countries—including USMCA partners exempted from prior measures—it erased hard-won regional trade advantages. Mexican auto exporters, who had invested heavily in nearshoring to avoid China-specific tariffs, suddenly faced identical duties on vehicles shipped from Monterrey and Guangzhou. This neutralization of geographic arbitrage undermined the very logic of supply chain diversification strategies pursued since 2022. Simultaneously, the tariff’s 150-day sunset clause created perverse incentives: importers rushed to front-load shipments in February and March 2026, causing container shortages in Asia and spiking spot freight rates by 140% on the Trans-Pacific corridor. Conversely, manufacturers delayed capital expenditures on automation upgrades, anticipating that tariff-induced cost pressures might ease—or escalate—if the administration followed through on its February 21 threat to raise the rate to 15%. This whiplash effect fractured long-term planning cycles: procurement teams abandoned traditional 12-month forecasting horizons in favor of rolling 90-day scenarios, while CFOs demanded real-time tariff exposure dashboards integrated with ERP systems.

Perhaps most revealing was Section 122’s impact on supplier relationships. Historically, U.S. buyers absorbed tariff costs to maintain pricing discipline; under Section 122, however, the blanket nature of the duty forced renegotiation of commercial terms across tiers. A major electronics distributor disclosed that 89% of its Asian suppliers demanded cost-plus adjustments, citing Section 122 as ‘force majeure equivalent’—a contractual stretch that exposed gaps in standard incoterms usage. Meanwhile, European pharmaceutical suppliers leveraged the tariff’s procedural vulnerability to demand ‘tariff indemnity clauses’ in distribution agreements, effectively transferring legal risk to U.S. importers. These developments signal a tectonic shift: tariffs are no longer external cost variables but embedded contractual mechanisms that redefine liability, payment terms, and intellectual property licensing frameworks. As one global supply chain consultant observed, ‘We’ve moved from managing tariffs to managing tariff risk as a core competency—like cybersecurity or ESG compliance.’

The Household Cost Conundrum: Why Tariffs Are Regressive Taxes in Disguise

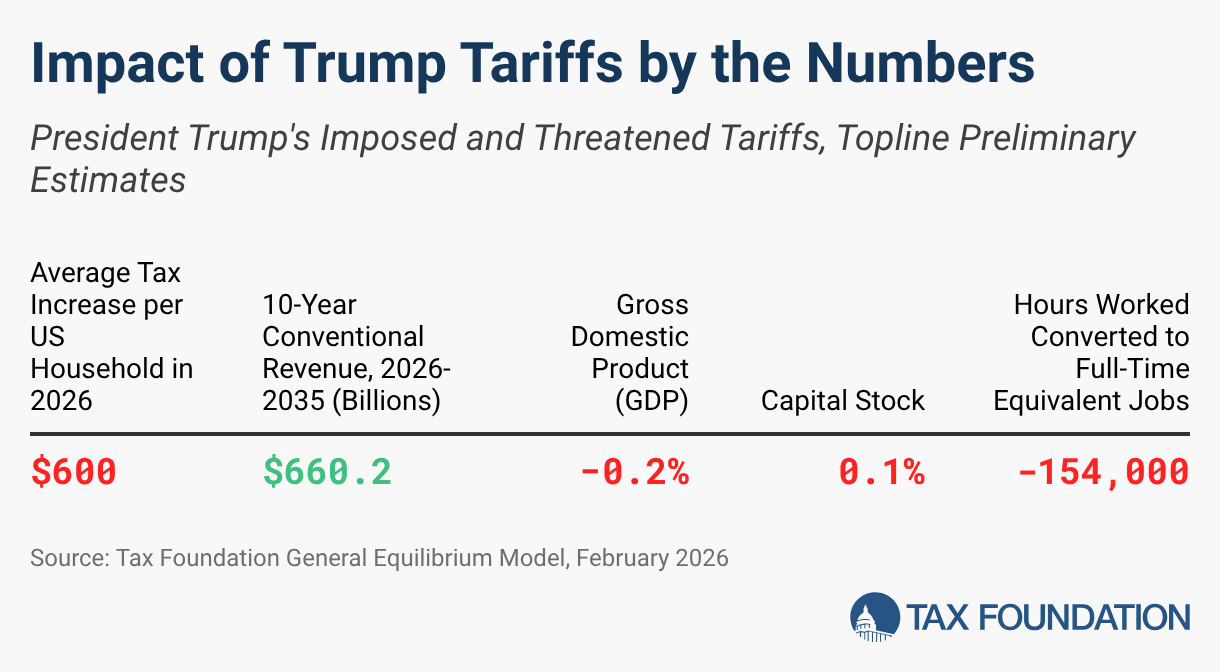

Conventional trade discourse treats tariffs as abstract instruments of statecraft, but their true impact registers first in household budgets. Tax Foundation estimates confirm that the 2025 IEEPA tariffs imposed a $1,000 annual burden per U.S. household, a figure derived from comprehensive modeling of price pass-through across 3,200 consumer product categories. This burden is profoundly regressive: households earning under $40,000 annually spent 12.7% of disposable income on tariff-affected goods (apparel, footwear, electronics), compared to just 3.4% for those earning over $150,000. The mechanism is unambiguous—tariffs raise landed costs, which retailers absorb partially but ultimately pass on through higher shelf prices, reduced promotions, and narrower product assortments. When Section 122’s 10% duty took effect, it added an estimated $200–$600 per household in 2026, compounding existing pressures from inflation and wage stagnation. Crucially, these figures represent direct consumer costs—not secondary effects like job losses in export-dependent sectors or reduced investment in tariff-vulnerable industries. The Congressional Budget Office corroborated this in its March 2026 analysis, finding that 92% of tariff incidence falls on domestic consumers, with only 8% borne by foreign exporters through lower export volumes.

This regressive impact reshapes retail supply chains at a fundamental level. Major discount retailers responded by accelerating private-label development programs, shifting sourcing from branded Asian manufacturers to contract producers in Vietnam and Bangladesh—markets not covered by Section 122’s initial implementation. Simultaneously, grocery chains expanded ‘tariff-free’ private brands for staples like canned goods and paper products, leveraging domestic co-packers to avoid duties entirely. These adaptations reveal a quiet revolution in category management: procurement teams now conduct ‘tariff elasticity studies’ alongside traditional demand forecasting, analyzing how price sensitivity varies across income brackets to determine optimal margin structures. For example, a national apparel retailer found that low-income shoppers exhibited 3.2x greater price elasticity for denim jeans than high-income cohorts, prompting targeted tariff-mitigation strategies—like shifting production of entry-level lines to Honduras—while maintaining premium lines sourced from Japan unaffected by Section 122. Such segmentation transforms supply chains from monolithic networks into modular, income-stratified architectures.

Moreover, the household cost calculus exposes a critical flaw in tariff-driven industrial policy: it assumes consumers will tolerate higher prices to support domestic manufacturing jobs. Yet labor data tells a different story. Between Q1 2025 and Q1 2026, manufacturing employment grew by just 0.4%, while retail and logistics jobs surged by 3.8%—many filled by workers displaced from tariff-impacted import-dependent sectors. This disconnect reveals that tariffs don’t automatically ‘bring back’ jobs; they relocate economic pain across the value chain. When a $499 smartphone becomes a $549 smartphone due to semiconductor tariffs, the extra $50 doesn’t fund new U.S. chip fabs—it funds port storage fees, customs brokerage, and working capital for importers navigating regulatory uncertainty. Thus, the household burden isn’t a side effect of trade policy; it’s the central transmission mechanism through which tariffs distort resource allocation, suppress aggregate demand, and ultimately constrain GDP growth—an effect the Tax Foundation quantifies as a 0.2% permanent reduction in U.S. GDP attributable solely to Section 232 measures, before accounting for foreign retaliation.

Trade Deficit Myths and Macroeconomic Realities: Why Tariffs Cannot Fix Structural Imbalances

Despite repeated assertions that tariffs would ‘eliminate the trade deficit,’ the data delivers a sobering verdict: the U.S. merchandise trade deficit fell by a mere $2.1 billion in 2025, driven entirely by a services surplus increase—not by reduced goods imports. This marginal change underscores a foundational truth obscured by political rhetoric: trade deficits are macroeconomic phenomena rooted in national savings-investment imbalances, not micro-level trade barriers. The United States consistently invests more than it saves, requiring capital inflows from abroad to finance the gap—capital inflows that manifest as trade deficits. As the Federal Reserve’s 2026 Financial Stability Report emphasizes, attempting to close the deficit via tariffs is akin to ‘stopping a river by damming individual tributaries’; it ignores the hydraulic pressure of global capital flows. When tariffs raise import prices, they reduce real household income, which depresses consumption—including of domestically produced goods—offsetting any theoretical boost to domestic manufacturing. Econometric analyses by the Peterson Institute confirm that tariff-induced import declines are consistently offset by reduced exports, as foreign trading partners retaliate and U.S. exporters face higher input costs.

This macroeconomic reality forces supply chain professionals to confront uncomfortable truths about resilience narratives. Nearshoring initiatives predicated on ‘deficit reduction’ goals have proven economically incoherent: relocating production from China to Mexico reduces tariff exposure but increases logistics costs by 18–22% due to infrastructure constraints, while failing to address the core drivers of U.S. trade imbalances. Instead, effective resilience requires financial engineering—hedging currency exposures, securing multi-currency credit facilities, and building balance sheet flexibility to absorb tariff volatility. The most sophisticated firms now treat tariffs as a stochastic variable in capital allocation models, assigning probability-weighted costs to different tariff scenarios when evaluating factory automation investments or M&A targets. For instance, a leading medical device company recently abandoned plans to build a U.S.-based assembly plant after modeling showed that Section 232 pharmaceutical tariffs would increase component costs by 27%, negating projected ROI—even with CHIPS Act subsidies.

Ultimately, the trade deficit debate distracts from what truly matters for supply chains: stability, predictability, and rule-of-law adherence. The Supreme Court’s IEEPA ruling, however politically inconvenient, restored a vital anchor—legal certainty. Firms can now design networks based on enforceable statutes rather than ephemeral executive orders. This shift elevates compliance from a cost center to a strategic capability: companies with robust trade legal functions are better positioned to identify tariff exemptions, navigate complex rules of origin, and leverage WTO dispute mechanisms. As global trade enters its next phase—not defined by bilateral tensions but by multilateral legal frameworks—the winners won’t be those who game the tariff system, but those who engineer supply chains resilient to its inherent volatility.

Strategic Implications: Building Post-Tariff Supply Chains in an Era of Legal Uncertainty

The 2026 tariff episode represents more than a policy reversal—it is a paradigm shift in how supply chains interface with sovereign power. Forward-looking organizations are abandoning reactive tariff mitigation in favor of proactive legal architecture: embedding tariff clauses in master service agreements, establishing regional tariff war rooms staffed by trade attorneys and economists, and developing ‘tariff scenario playbooks’ approved by board audit committees. These aren’t theoretical exercises; they’re operational necessities. When Section 122’s 150-day clock began ticking, leading aerospace firms activated pre-negotiated ‘tariff suspension protocols’ with Tier 2 suppliers, allowing temporary cost-sharing arrangements that preserved cash flow without breaching commercial contracts. Similarly, pharmaceutical distributors implemented AI-driven tariff classification engines that cross-reference HS codes with real-time court rulings, automatically flagging high-risk shipments for legal review before customs entry. This fusion of legal expertise and digital infrastructure signals a new supply chain competency—one where compliance officers sit alongside CTOs in technology investment decisions.

Geopolitically, the judicial reset accelerates the fragmentation of global trade governance. With U.S. unilateralism curtailed, the EU and ASEAN are fast-tracking mutual recognition agreements for conformity assessments, reducing reliance on U.S.-centric certification pathways. Meanwhile, China is leveraging the U.S. legal crisis to promote its ‘Digital Silk Road’ standards framework, offering tariff-free digital trade corridors to countries adopting its e-commerce interoperability protocols. For U.S. firms, this means supply chain strategy can no longer be siloed within national borders; it must anticipate divergent regulatory regimes across jurisdictions. A single semiconductor fab may need to comply with U.S. export controls, EU Digital Product Passports, and Vietnamese customs valuation rules—all governing different aspects of the same physical good. This complexity rewards firms with deep institutional knowledge of comparative administrative law, not just logistics expertise.

Looking ahead, the enduring lesson of 2026 is that supply chain resilience is inseparable from constitutional resilience. The Supreme Court didn’t just strike down tariffs—it reaffirmed that sustainable trade policy requires legislative deliberation, evidentiary rigor, and judicial oversight. Companies that treat tariffs as transient political noise do so at their peril; those that integrate legal uncertainty into core strategy will emerge as the architects of the next-generation supply chain: one built not on protectionist walls, but on transparent, accountable, and legally durable foundations. As the Tax Foundation concludes, the era of ’emergency’ trade policy is over—not because threats have vanished, but because democracy reclaimed its institutional boundaries. The supply chains that thrive in this new reality won’t be the shortest or cheapest, but the most legally literate.

Source: taxfoundation.org