A Landmark Risk Assessment Reframes South America’s Strategic Role

In February 2026, risk consultancy Verisk Maplecroft published what may prove to be one of the most consequential supply chain intelligence reports of the year. By systematically evaluating 10 emerging markets with major reserves of cobalt, copper, graphite, lithium, nickel, and rare earth elements, the firm delivered a clear verdict: South American nations exhibit “comparatively lower resource nationalism risk” and could be “key” to the West’s restructuring of critical minerals supply chains. The countries assessed — Argentina, Brazil, Chile, the Democratic Republic of the Congo (DRC), India, Indonesia, Madagascar, Peru, the Philippines, and Tanzania — span every major resource-rich region on the planet, making the findings a genuine global benchmark.

The timing could not be more significant. The world is navigating the most profound supply chain realignment since the Cold War, with critical minerals at its epicenter. From electric vehicle batteries to semiconductor manufacturing, from renewable energy infrastructure to defense systems, these materials underpin the technologies that will define economic competitiveness and national security for decades to come. China currently controls 60-70% of global rare earth mining and 85-90% of processing capacity, a concentration that Western governments have belatedly recognized as a strategic vulnerability of the first order. Against this backdrop, Verisk Maplecroft’s assessment elevates South America from a peripheral player to a central pillar of the emerging post-China minerals architecture.

Decoding the Resource Nationalism Index: What Sets South America Apart

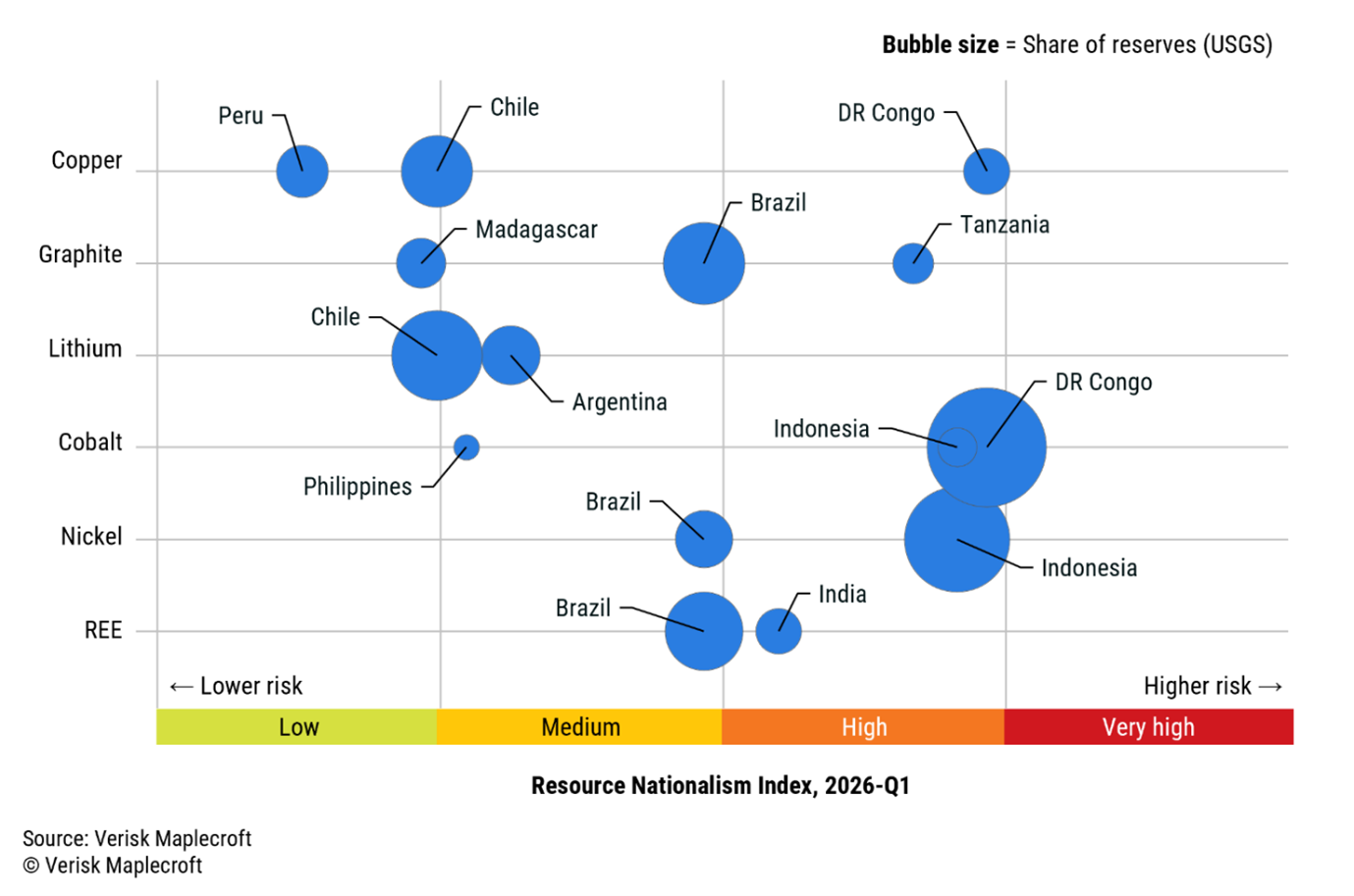

Maplecroft’s methodology centers on its proprietary resource nationalism index, which quantifies the degree of government control over extractive-sector economic activity — encompassing taxation regimes, state ownership mandates, export restrictions, and regulatory unpredictability. The results reveal a stark geographic divide: the DRC, Indonesia, and Tanzania all rank within the global top 20 highest-risk environments for resource nationalism, while Peru, Chile, and Argentina occupy markedly lower positions on the risk spectrum.

Chief analyst Jimena Blanco attributed this divergence to the “distribution of risk” that sets South America apart, noting it explains “the intensifying US and EU focus” on the region. Simon Wolfe, co-founder of geopolitical advisory firm Marlow Global, reinforced this assessment with a practitioner’s perspective: South American jurisdictions possess “reliable legal systems, the rule of law, established mining frameworks, and long track records of hosting international operators.” Most critically for investors with multi-decade horizons, the ability to “enforce contracts and repatriate capital” distinguishes the region — “asset seizures common in other regions are rare in South America.” For mining operations that may not generate returns for a decade or more, this institutional stability is not merely reassuring; it is a prerequisite for capital deployment at scale.

The Lithium Triangle and the Copper Corridor: A Resource Endowment Without Parallel

South America’s centrality in the critical minerals conversation rests on geological foundations that no amount of political maneuvering can replicate elsewhere. The Lithium Triangle — spanning Argentina, Bolivia, and Chile — contains approximately half of the world’s known lithium resources. As the essential raw material for lithium-ion batteries powering electric vehicles and grid-scale energy storage, lithium has been described as “the new oil” of the energy transition. Meanwhile, Chile and Peru together produce more than one-third of global copper output, a metal whose demand is being supercharged by renewable energy deployment, electrical grid modernization, and the explosive growth of AI-driven data centers.

Brazil adds another critical dimension. The country holds the world’s second-largest rare earth reserves and produces approximately 90% of global niobium — a metal essential for high-strength, low-alloy steels used in aerospace and energy infrastructure. In a landmark deal, the US International Development Finance Corporation (DFC) committed $565 million in financing to Brazilian rare earths miner Serra Verde, one of the largest single US investments in Latin American mining. This transaction signals that Washington views Brazil not merely as a commodity supplier but as a strategic node in the Western minerals supply network — a distinction that carries profound implications for trade flows, logistics infrastructure, and regional power dynamics.

The Western Offensive: Project Vault, FORGE, and the Race to Secure Supply

Western governments are backing their strategic assessments with unprecedented financial and diplomatic commitments. The Trump administration’s Project Vault, supported by the US Export-Import Bank (EXIM), aims to establish strategic mineral stockpiling facilities across the United States, creating a buffer against supply disruptions. This initiative operates in concert with the FORGE alliance, a 55-nation coalition convened by Washington to coordinate the diversification of critical minerals supply chains away from Chinese dominance. Notably, Argentina, Bolivia, Brazil, and Peru all participated in the US 2026 Critical Minerals Ministerial, underscoring the region’s active engagement in this global restructuring.

The United Kingdom has pursued a parallel track. UK Export Finance (UKEF) has introduced the Critical Goods Export Development Guarantee, and the UK business secretary stated this month that a critical minerals alliance among major economies “makes sense.” The European Union’s Critical Raw Materials Act establishes binding domestic targets for extraction, processing, and recycling by 2030. Olena Borodyna, senior geopolitical risks advisor at ODI Global, noted that the region’s engagement “is reflected in both diplomatic and financial terms” but cautioned that US intervention in Venezuela and broader regional policy could complicate bilateral relationships and introduce new categories of political risk for American investors operating in the hemisphere.

Resource Nationalism’s Shadow: Why ‘Lower Risk’ Is Not ‘No Risk’

Marlow Global’s Wolfe issued a critical caveat that supply chain strategists would be wise to heed: “Less risky than the alternatives is not the same as safe.” Resource nationalism is gaining momentum across South America, and each major producer presents its own distinct risk profile. Chile now requires state majority stakes in new lithium partnerships, effectively positioning international investors as junior partners. Bolivia has fully nationalized its lithium sector, virtually shutting out private capital. Argentina’s Incentive Regime for Large Investments (RIGI) offers 30 years of fiscal and regulatory stability — an attractive proposition on paper, but one shadowed by “decades of policy reversals” that continue to weigh on investor confidence.

Community-level opposition presents an additional and growing challenge. In Chile and Peru, local populations and environmental organizations are intensifying resistance to mining expansion, driven by concerns over water depletion, soil contamination, and ecosystem destruction. These social risks can delay project approvals by years or result in outright cancellation. For supply chain planners, this means that South America’s mineral development timelines may be substantially longer than geological assessments suggest, and the gap between “reserves on paper” and “commercially accessible supply” remains vast. As Maplecroft’s Blanco concluded, success will require “integrating geopolitical foresight, resource nationalism and political risk assessment to delineate the clearest pathway to building resilient, western-aligned critical mineral supply chains.”

India-Brazil Minerals Diplomacy and the Emerging Global Architecture

The critical minerals reshaping extends well beyond the Western alliance framework. On February 21, 2026, Indian Prime Minister Modi and Brazilian President Lula signed a bilateral cooperation agreement on critical minerals and rare earths in New Delhi. Modi described the pact as “a big step in building resilient supply chains,” while Lula characterized cooperation in renewable energy and critical minerals as “at the core of the pioneering agreement” the two leaders concluded. Brazil presented data on its world-second-largest rare earth reserves, noting that a significant portion remains unexplored — suggesting substantial upside potential for development partnerships.

This India-Brazil axis represents a new vector in global minerals diplomacy that operates partly independently of Western alliance structures. Viewed alongside the US-led FORGE coalition, the EU’s Mercosur trade negotiations, and bilateral deals proliferating across the Global South, a picture emerges of a multipolar competition for mineral access that will reshape trade routes, logistics networks, and geopolitical alignments for years to come. South America’s critical minerals story is still in its earliest chapters, but its implications for global supply chain architecture will reverberate through the next decade and beyond.

Source: Global Trade Review