According to en.sedaily.com, Qatar’s force majeure declaration on liquefied natural gas (LNG) supplies has triggered cascading disruptions across South Korea’s semiconductor, steel, and shipping sectors — with helium supply emerging as a critical vulnerability.

Helium Shortage Threatens Semiconductor Production

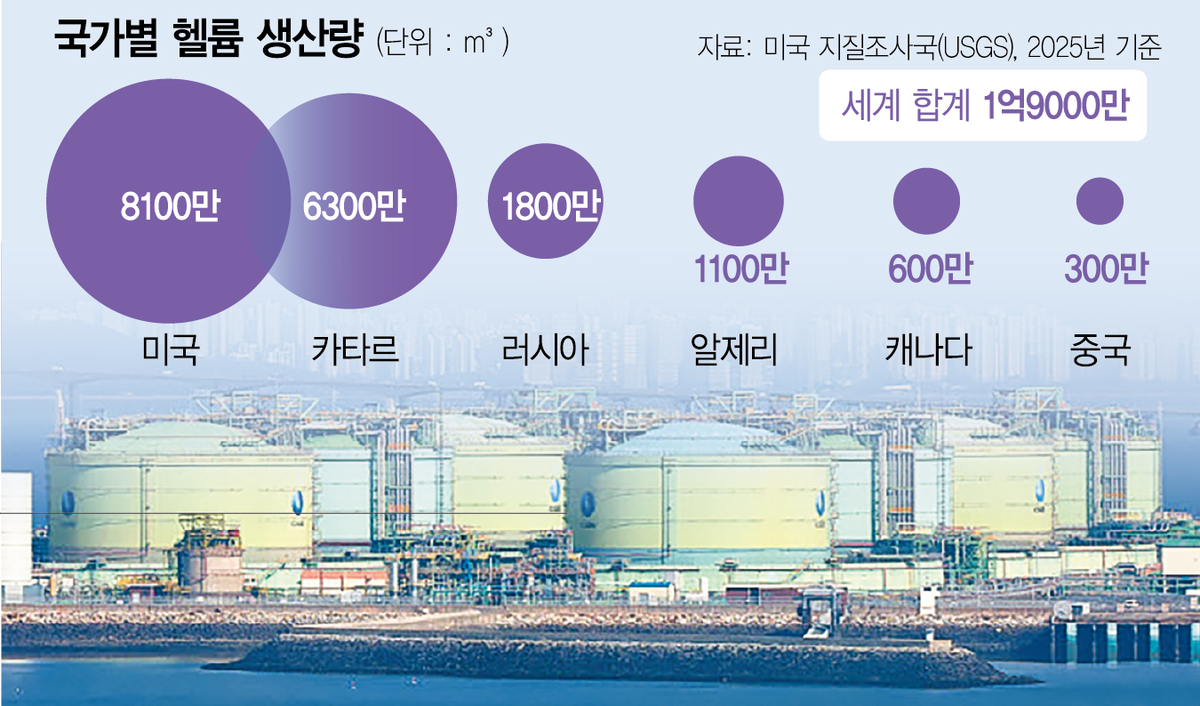

Helium — essential for wafer cooling and precision processes in advanced chip manufacturing — is produced as a byproduct of LNG refining. With South Korea importing 65% of its helium from Qatar, the disruption carries acute risk. The Ras Laffan LNG facility, where the force majeure was declared, accounts for one-third of global helium supply, according to IBK Investment & Securities.

Domestic semiconductor firms currently hold approximately six months’ worth of helium inventory and report having secured alternative suppliers. However, market conditions are deteriorating rapidly: helium spot prices have surged 100% in just two weeks. This volatility threatens continuity in high-end manufacturing, particularly for AI infrastructure buildout.

“If the dispute drags on, it could escalate into a bottleneck risk for advanced semiconductor manufacturing and AI infrastructure buildout.” — Lee Dong-wook, researcher at IBK Investment & Securities

Steel and Energy Use Under Pressure

South Korean steelmakers rely on LNG not only for captive power generation but also as a raw material input. Hyundai Steel uses LNG to generate electricity at its Dangjin steelworks. POSCO, while primarily powered by blast furnace byproduct gases, also incorporates LNG in select operations. Any sustained LNG shortage may force operational adjustments — including fuel substitution or reduced output — especially during peak energy demand periods.

Shipping Contracts Face Geopolitical Exposure

Korean shipping firms with long-term charters to QatarEnergy face uneven exposure. Pan Ocean (028670.KS), H-Line Shipping, and SK Shipping each operate five vessels — totaling 15 LNG carriers — under fixed-fee charters. Most contracts guarantee charter fees regardless of cargo loading. However, one SK Shipping vessel positioned inside the Strait of Hormuz faces potential contract termination — a direct consequence of escalating regional tensions.

Broader implications include increased working capital burdens if alternative shipping routes (e.g., longer detours around the Red Sea or Persian Gulf) become necessary. Such shifts could strain cash flow during scheduled loan principal and interest repayments for ship financing.

Geopolitical Toll Shifts Cost Calculus

The crisis coincides with Iran’s reported introduction of transit fees of up to $2 million (≈3 billion won) per passage through the Strait of Hormuz — effective Saturday local time. This undermines the longstanding economic rationale for Middle Eastern energy imports, which had relied on shorter distances and historically lower transport costs compared to North American or African alternatives.

Analysts stress that even a temporary ceasefire brokered via U.S.-Iran negotiations would not eliminate structural risk: energy infrastructure in the region remains vulnerable to recurring instability. As a result, long-term energy supply contracts with Middle Eastern counterparties now carry heightened counterparty and delivery risk.

Source: en.sedaily.com

Compiled from international media by the SCI.AI editorial team.