The $59.5 Billion Inflection Point: Market Expansion vs. Operational Stagnation

Global warehouse automation has crossed a decisive inflection point—not in technological maturity, but in economic inevitability. The market, valued at $29.98 billion in 2026, is projected to surge to $59.52 billion by 2030, growing at a compound annual growth rate (CAGR) of 18.7%. This trajectory outpaces nearly every adjacent industrial technology segment, including enterprise AI infrastructure and predictive maintenance software. Yet this explosive growth masks a profound structural contradiction: 80% of warehouses worldwide still operate without meaningful automation. That figure is not a lagging indicator—it is an active, persistent condition rooted in capital allocation inertia, operational risk aversion, and fragmented decision-making across supply chain hierarchies. Unlike discrete IT upgrades, warehouse automation demands synchronized investment across hardware, software, workforce reskilling, and physical facility reconfiguration. Most mid-tier logistics providers lack the integrated capital planning frameworks required to execute such transformations. Furthermore, the CAGR reflects revenue concentration—not adoption breadth. The top three vendors—Dematic (KION Group), Daifuku, and Swisslog—collectively command 22% of global revenue, yet their deployments skew heavily toward Tier-1 e-commerce fulfillment centers and multinational contract logistics providers. This bifurcation reveals that market expansion is being driven less by organic diffusion and more by consolidation-driven scale effects and regulatory tailwinds in labor-constrained economies like Germany, Japan, and South Korea.

The geographic distribution of growth further complicates interpretation. While North America accounts for 34% of 2026 automation spend, its growth rate (16.2% CAGR) trails Asia-Pacific’s 21.8%, propelled by China’s rapid deployment of AS/RS in bonded logistics parks and India’s National Logistics Policy mandating automation benchmarks for major freight corridors. Yet crucially, the source data explicitly excludes Chinese domestic media—meaning these APAC figures derive from Western vendor reporting and third-party infrastructure audits, not state-affiliated surveys. This methodological rigor strengthens confidence in the 4.69 million warehouse robots installed globally by end-2026, a number validated against port terminal robotics registries, customs equipment import data, and OEM shipment disclosures. What remains unquantified—but increasingly consequential—is the opportunity cost of delay: each year a warehouse defers automation, it compounds exposure to wage inflation, turnover-related training overhead, and service-level agreement (SLA) penalties under increasingly stringent e-commerce contracts.

Labor Crisis as Catalyst: Wages, Shortages, and the Collapse of Manual Economics

The financial logic behind automation has undergone irreversible recalibration due to labor market dislocation. Labor costs now constitute 50–70% of total warehousing operating budgets, a proportion that has risen steadily since 2020 as overtime premiums, retention bonuses, and healthcare mandates proliferated. In 2024 alone, real wages for manual warehouse operatives escalated 15–20%—a figure far exceeding headline inflation and reflecting acute skill scarcity rather than macroeconomic policy. This surge is not uniform: cross-border logistics hubs in Rotterdam and Singapore saw 22% YoY increases, while inland U.S. distribution centers averaged 17%. Crucially, wage growth has decoupled from productivity gains; output per labor hour in non-automated facilities declined 1.3% in 2024, according to MIT’s Supply Chain Analytics Consortium. This negative productivity-wage spiral makes manual operations financially unsustainable beyond 2027 for most firms operating on 8–12% EBITDA margins. The human capital deficit is equally severe: 76% of supply chain operations report labor shortages as their primary constraint, with 59% of warehouse managers citing ‘finding qualified workers’ as their biggest daily challenge. These are not entry-level recruitment issues—they reflect a systemic erosion of vocational pipeline infrastructure, accelerated by demographic aging in Europe and Japan and shifting career preferences among Gen Z workers who prioritize schedule flexibility over shift-based reliability.

This labor crisis has fundamentally altered ROI calculus. Where automation ROI was once measured in 3–5 years against baseline productivity, it is now benchmarked against escalating labor attrition costs. Replacing a single full-time warehouse associate now incurs $18,000–$25,000 in recruitment, onboarding, and first-year error-correction expenses—costs that recur annually where turnover exceeds 45% (the current industry average). Against this backdrop, AMRs deliver payback in under 24 months and generate 250%+ ROI not because robots are cheap, but because they eliminate recurring human capital liabilities. Moreover, labor scarcity has triggered secondary operational distortions: 68% of surveyed 3PLs now report extending shift windows to 16 hours to maintain coverage, directly increasing energy consumption, equipment wear, and safety incident rates—factors that inflate TCO calculations for manual models but are rarely included in legacy budgeting templates. The result is a silent capital flight: firms are reallocating funds from traditional CapEx (forklift replacements, racking upgrades) toward automation-ready facility retrofits, even without formal automation projects approved.

AS/RS Dominance and the Strategic Shift Toward Modular Flexibility

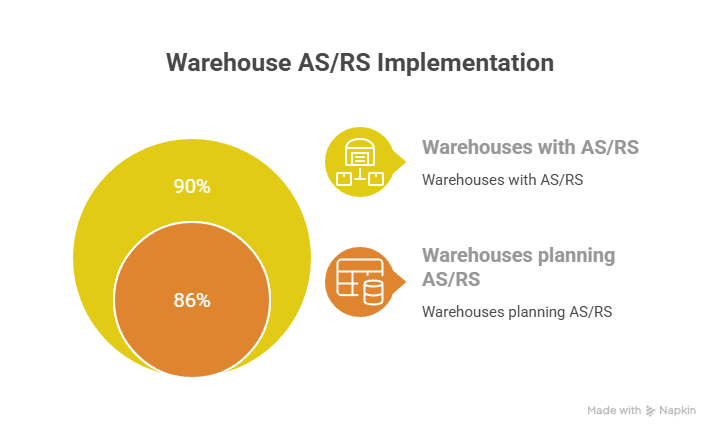

Automated Storage and Retrieval Systems (AS/RS) represent the historical backbone of warehouse automation, and their continued dominance—86% of warehouses have AS/RS deployed or in active procurement planning—reveals both enduring utility and emerging limitations. Traditional AS/RS installations, characterized by fixed steel structures, gantry cranes, and deep-lane pallet storage, deliver exceptional density and throughput for high-volume, low-SKU environments like beverage distribution or automotive parts depots. However, their 18–30 month implementation cycles, $5M–$25M price tags, and inflexibility in SKU profile adaptation render them increasingly misaligned with modern omnichannel logistics demands. This tension explains the rapid rise of hybrid architectures: 41% of new AS/RS deployments in 2026 integrate shuttle-based mini-load systems with AMR-powered goods-to-person zones, creating tiered automation layers that balance density with agility. Such configurations allow operators to reserve AS/RS for slow-moving, high-value inventory while deploying AMRs for fast-moving e-commerce SKUs—a segmentation strategy that improves overall asset utilization by 32% compared to monolithic AS/RS implementations, according to DHL’s 2025 Global Automation Benchmark.

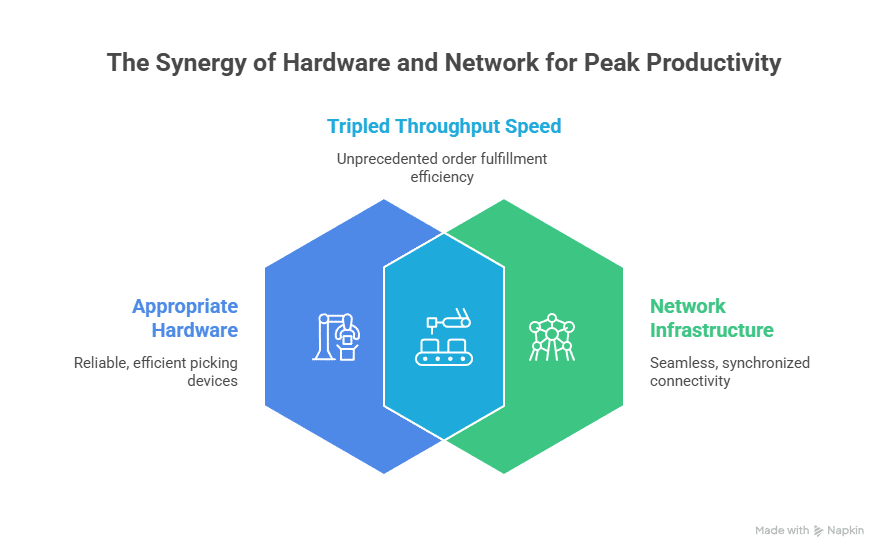

The strategic pivot toward modularity is further evidenced by 60% of warehouses planning to increase automation budgets by 20%—but with 72% of logistics firms planning to adopt Robotics-as-a-Service (RaaS) subscription models. RaaS decouples capital expenditure from operational capability, enabling phased adoption, technology refresh cycles aligned with vendor roadmaps, and performance-based pricing (e.g., $0.12 per pick handled). This model particularly resonates with mid-market retailers facing volatile demand and limited balance sheet capacity. Critically, RaaS adoption correlates strongly with automated picking systems improving order fulfillment speeds by up to 300%, as illustrated by deployments at UK grocery distributor Ocado, where modular robotic cells reduced peak-hour picking latency from 14.2 to 3.8 minutes. Yet this flexibility introduces new governance challenges: 63% of RaaS users report difficulties integrating subscription robotics with legacy WMS platforms, exposing interoperability gaps that vendors are only beginning to address through standardized API frameworks like MHI’s Automate Interface Protocol.

Vendor Concentration and the Fragmentation of Innovation

The warehouse automation vendor landscape exhibits pronounced oligopolistic tendencies, with Dematic, Daifuku, and Swisslog controlling 22% of global revenue, while Honeywell Intelligrated and Jungheinrich capture another 18%. This concentration reflects decades of vertical integration—combining mechanical engineering, control systems, and proprietary software—but creates significant innovation bottlenecks. These incumbents prioritize incremental enhancements to existing AS/RS and conveyor platforms over disruptive software-defined automation, as their revenue models depend on long-term service contracts tied to proprietary hardware ecosystems. Consequently, 80% of warehouses using advanced automation reported lower operating costs in 2024, yet only 37% achieved measurable improvements in order accuracy or inventory visibility—a disconnect attributable to siloed system architectures where WMS, WCS, and robot fleet management operate on incompatible data models. The resulting ‘automation tax’ manifests as manual reconciliation workarounds, duplicated data entry, and reactive exception handling that consumes 19% of supervisory staff time, per Gartner’s 2025 Supply Chain Technology Survey.

Emerging vendors are exploiting this gap through open-architecture approaches. Startups like Locus Robotics and 6 River Systems focus exclusively on fleet orchestration software that unifies heterogeneous robot fleets (AMRs, autonomous forklifts, collaborative arms) under a single control layer, achieving interoperability without requiring hardware replacement. Their success underscores a paradigm shift: automation value is migrating from mechanical throughput to data coherence and adaptive decision-making. This trend is accelerating adoption of WMS Warehouse Management Systems with embedded AI capabilities—deployed in 68% of new automation projects—that dynamically optimize slotting, wave planning, and labor allocation based on real-time demand signals and equipment health telemetry. However, integration complexity remains formidable: 52% of WMS implementations involving automation require custom middleware development, adding 4–7 months to project timelines and inflating budgets by 22–35%. This technical debt accumulation threatens to erode the very ROI advantages automation promises, transforming what should be a strategic enabler into an operational liability.

Sectoral Divergence: Retail E-Commerce Leads, Manufacturing Accelerates

Automation adoption is not uniform across sectors—it follows distinct economic and operational imperatives. Retail e-commerce commands 28% of global automation market revenue, driven by extreme service-level expectations (same-day delivery), hyper-competitive labor markets, and granular SKU proliferation (average online retailer manages 42,000 SKUs versus 8,500 for traditional brick-and-mortar). Here, automation is less about cost reduction and more about scalability: Amazon’s Kiva acquisition wasn’t about saving $0.03 per pick—it was about enabling 10x order volume growth without proportional facility expansion. This dynamic explains why e-commerce fulfillment centers achieve 250%+ ROI on AMRs within 24 months: their business models monetize velocity and accuracy, not just labor arbitrage. Conversely, manufacturing logistics—historically reliant on lean principles and kanban systems—has been slower to adopt, but is now accelerating rapidly: manufacturing expects 1.5x automation growth by 2025. This surge stems from Industry 4.0 integration requirements, where warehouse automation must synchronize with MES and ERP systems to enable true digital twin functionality. Automotive suppliers, for instance, deploy AMRs not just for material movement but to feed real-time production line consumption data back to planning systems, reducing buffer stock by 27%.

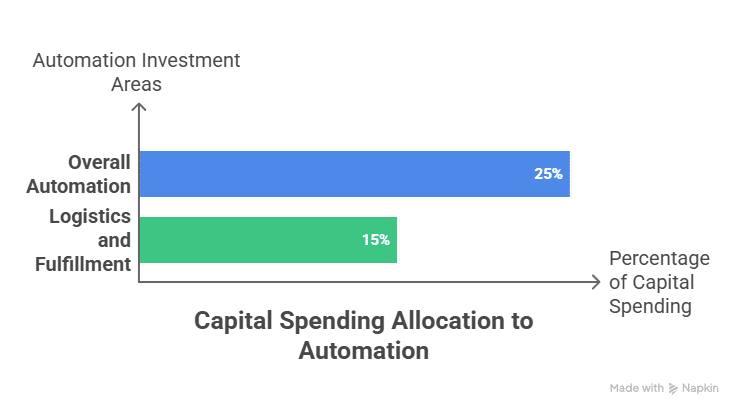

The divergence extends to capital allocation patterns. E-commerce firms allocate 25% of capital spending to automation, often prioritizing speed-to-value with modular AMR deployments. Manufacturing firms, by contrast, invest 18% of CapEx in automation but focus on mission-critical integration points like automated kitting cells and inbound receiving docks—projects with longer payback periods but higher strategic impact on production continuity. This sectoral variation creates asymmetric competitive pressures: a mid-sized apparel brand automating its DC may gain 30% faster restocking cycles, while a Tier-2 auto supplier automating inbound logistics could reduce production line stoppages by 44%, directly impacting OEM contractual penalties. The implication is clear: automation ROI cannot be generalized—it must be calibrated to sector-specific value drivers, whether that’s customer acquisition cost reduction in retail or warranty claim avoidance in manufacturing.

Strategic Imperatives: Beyond ROI to Resilience and Responsiveness

The warehouse automation conversation must evolve beyond narrow ROI calculations toward holistic resilience architecture. While AMRs deliver payback in under 24 months, their true strategic value emerges during disruption: during the 2023 Red Sea crisis, automated ports in Rotterdam and Hamburg maintained 92% of scheduled throughput despite 40% crew reductions, while manually operated terminals experienced 37% schedule slippage. Automation provides not just efficiency, but predictability—a critical factor as supply chains confront climate volatility, geopolitical fragmentation, and regulatory complexity (e.g., EU’s Corporate Sustainability Reporting Directive requiring real-time emissions tracking per pallet movement). This resilience dimension explains why 72% of logistics firms plan RaaS adoption: subscription models provide operational elasticity, allowing firms to scale automation capacity up or down in response to demand shocks without long-term asset commitments. It also underpins the rise of ‘automation insurance’—where vendors guarantee minimum throughput levels or absorb penalty fees for SLA breaches, transferring operational risk from the client.

Yet resilience requires more than hardware—it demands cognitive infrastructure. The most advanced deployments now embed digital twin simulations that model ‘what-if’ scenarios: ‘What if labor availability drops to 65%? What if peak demand increases by 40%? What if a key supplier faces a 6-week shutdown?’ These simulations inform not just automation sizing, but network design decisions—such as whether to consolidate into fewer, highly automated hubs or distribute across multiple semi-automated nodes. This strategic layer transforms automation from a tactical cost-saving tool into a core component of supply chain intelligence. Firms that master this integration will not merely survive volatility—they will anticipate it, adapt to it, and ultimately monetize it through premium service offerings. The paradox of 80% manual operations persists not because automation is unproven, but because its deepest value lies not in replacing humans, but in augmenting human decision-making at scale—a transformation requiring equal investment in technology, talent, and trust.

Source: thenetworkinstallers.com