Fastenal: Robust Business Model, but Limited Margin of Safety

Author: Kenio Fontes

The company’s solid business model and dividend growth stand out, but high valuations limit short-term upside and margin of safety.

Summary

- Fastenal’s business model, including on-site services, enhances operational efficiency and revenue growth, positioning it as a key player in industrial distribution.

- The stock’s high valuation multiples constrain short-term appreciation, with cyclical pressures and economic uncertainties impacting its profit growth potential.

- Despite Fastenal maintaining a strong dividend track record, the high premium reduces margin of safety, affecting future investor returns.

Typically, in equity investments, we look for companies with strong brand power, differentiation, and significant entry barriers. However, Fastenal Co. (FAST) does not fit this mold. Operating in the industrial supplies distribution sector, it has low differentiation and relatively low entry barriers.

Nevertheless, the company compensates for this by efficiently executing its business model, offering diversified solutions and inventory management services, along with a vast distribution network, which provides some competitive advantage.

Consequently, Fastenal boasts an enviable record of progressively improving financial health, thereby delivering shareholder value.

Despite being a very robust and attractive company, there are two primary risks to monitor. The first is the cyclical risk in its market. The second is valuation, which is only marginally acceptable under base-case scenarios.

Strategic Evolution Driving Continuous Growth and Operational Efficiency

Fastenal is a broad distributor of industrial and construction products, including safety materials, fasteners, and other tools and equipment. It also assists customers with inventory management and cost reduction efforts.

In recent years, Fastenal has expanded its on-site engagement strategy through initiatives like FastBin and FastVend. This approach benefits both parties. For Fastenal, it expands and builds customer loyalty (improving relationships), enhances operational efficiency via automated sales and better logistics, and makes revenue more recurring. For customers, it optimizes inventory costs, making management simpler and more efficient while providing quick access to needed materials.

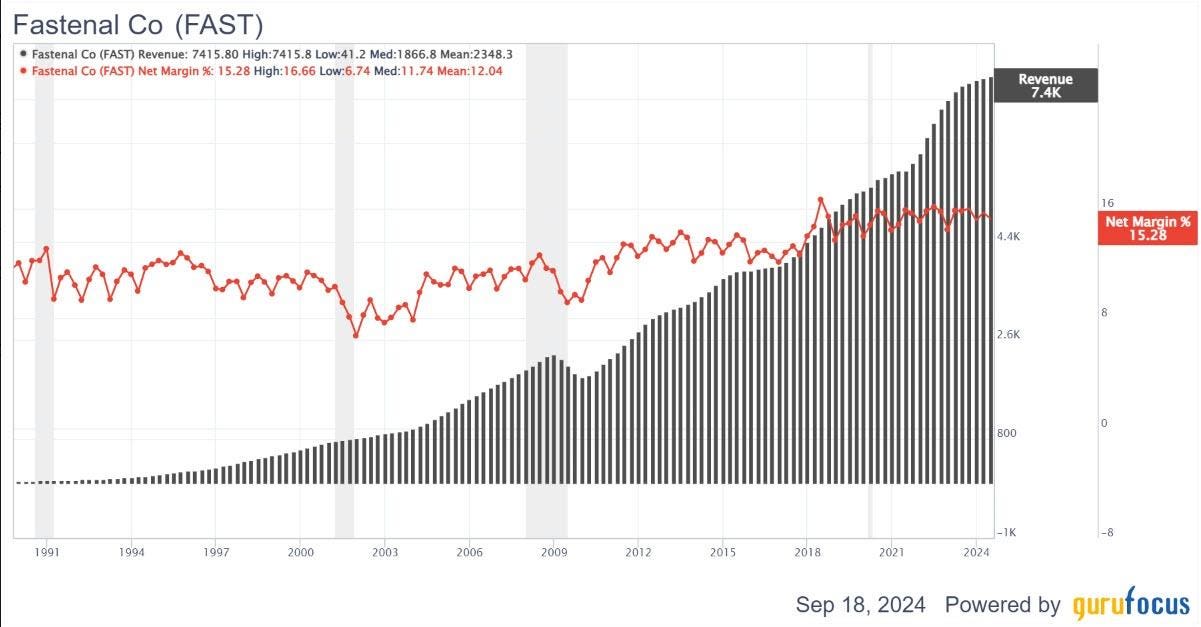

Over the past few years, the company has reduced its branch count while expanding on-site locations. In 2014, Fastenal had 214 on-site locations with on-site revenue of $387 million, representing nearly 10% of total net sales. By 2023, this number increased to 1,822 sites (rising to 1,934 by the second quarter), accounting for about 40% of its revenue.

Notably, this business model combined with strong execution has delivered solid financial performance. Even in a cyclical industry, good management has consistently improved net income and net profit margins. While growth rates have slowed in recent quarters, profitability faces greater challenges. Management noted that customer sentiment remains challenging, including the U.S. Purchasing Managers’ Index declining to 48.80 in Q2, though this was partly offset by better client acquisition and contract growth.

Despite the increasing weight of on-site operations, challenging scenarios, and some inefficiencies in the short-term supply chain have led to a 0.40 percentage point decline in gross margin year-over-year to 45.10%, with operating margins falling from 21% to 20.20%, impacted by increased selling, general, and administrative expenses. Nonetheless, Fastenal emphasizes its continued caution and plans to maintain strict cost control into Q3.

Long-term, this slightly challenging period is almost negligible, especially considering the steady increase in dividends per share, which continues to grow gradually and steadily with strong support from earnings growth. On the other hand, diluted earnings per share growth has slowed due to the aforementioned factors.

Overall, these earnings translate into cash generation, supporting strong returns to shareholders through dividend growth and buybacks. Notably, with minimal capital expenditure needs, this also makes distributions healthier and more predictable.

Finally, the company’s capital structure is quite comfortable. Beyond generating substantial cash flow, its debt exceeds $500 million, while cash and equivalents exceed $250 million. With very low leverage, significant principal repayments or interest expenses are not required.

In summary, Fastenal has a solid track record in execution. Its effective management strategies and cost-cutting measures have demonstrated consistent and sustainable returns despite operating in a cyclical market with no clear entry barriers.

Valuation Concerns

The issue lies in the high premium already attributed to the stock by the market. This premium is even higher during challenging periods for Fastenal, as short-term economic activity growth remains uncertain despite interest rate cuts and some statements about economic resilience, leading to concerns over future quarterly growth.

Specifically, Fastenal’s valuation multiples are: forward P/E of 33.30, forward EV/EBITDA of 23.20, and price-to-operating cash flow of 29.80. All these multiples significantly exceed their medians.

However, multiples are relative. A forward P/E of 33 may not be excessive for a company with high-quality fundamentals and forecasted accelerated growth. However, I do not believe Fastenal fully fits this profile. As previously mentioned, its business model and execution record are excellent, but analysts’ forecasts for the next few years do not show such robust growth. By 2026, market consensus expects Fastenal’s earnings per share to reach $2.40 — a sustainable and reasonable growth from $2.02 in 2023 — even so, this still implies a P/E of over 29 by 2026.

Paying such a premium diminishes shareholder returns as the dividend yield is relatively low compared to higher payout ratios. Based on projected earnings per share for 2026, if the company pays out 80%, the current yield would be 2.70%, still below the average historical dividend yield of 3.15% over the past ten years and will take two more years to achieve.

Given the company is in a challenging cycle, earnings are under pressure, and recovery could be favorable for Fastenal, especially if combined with internal cost optimization initiatives and more revenue from on-site operations. This not only may restore revenue growth but also continue to gradually improve net profit margins.

Even in this scenario, it still requires believing the company will accelerate its free cash flow growth rate and discount this cash flow at very low rates. In a discounted cash flow model, considering an 11% growth rate over the next two decades and discounting at 7%, we find Fastenal’s fair price to be only $60. In other words, while this valuation is reasonable, I do not consider it attractive. Although I believe the company’s outlook is positive and reliable, an annual growth of 11% already well incorporates such optimism, eroding the margin of safety.

Conclusion

Fastenal is a great company worthy of continuous attention as a solid choice for compound growth. Its efficient management enables it to create good value for shareholders with promising prospects for sustainable cash flow growth and being a reliable dividend payer, making it an ideal option for investors seeking high-quality income alternatives.

On the other hand, current stock prices are somewhat overvalued even though recent performance has been relatively flat. This is why I believe a more cautious approach is needed, waiting for a higher margin of safety before entering or increasing holdings.

Disclosure

I/we have no positions in any stocks mentioned and do not have any plans to initiate new positions within the next 72 hours.

Source: Forbes