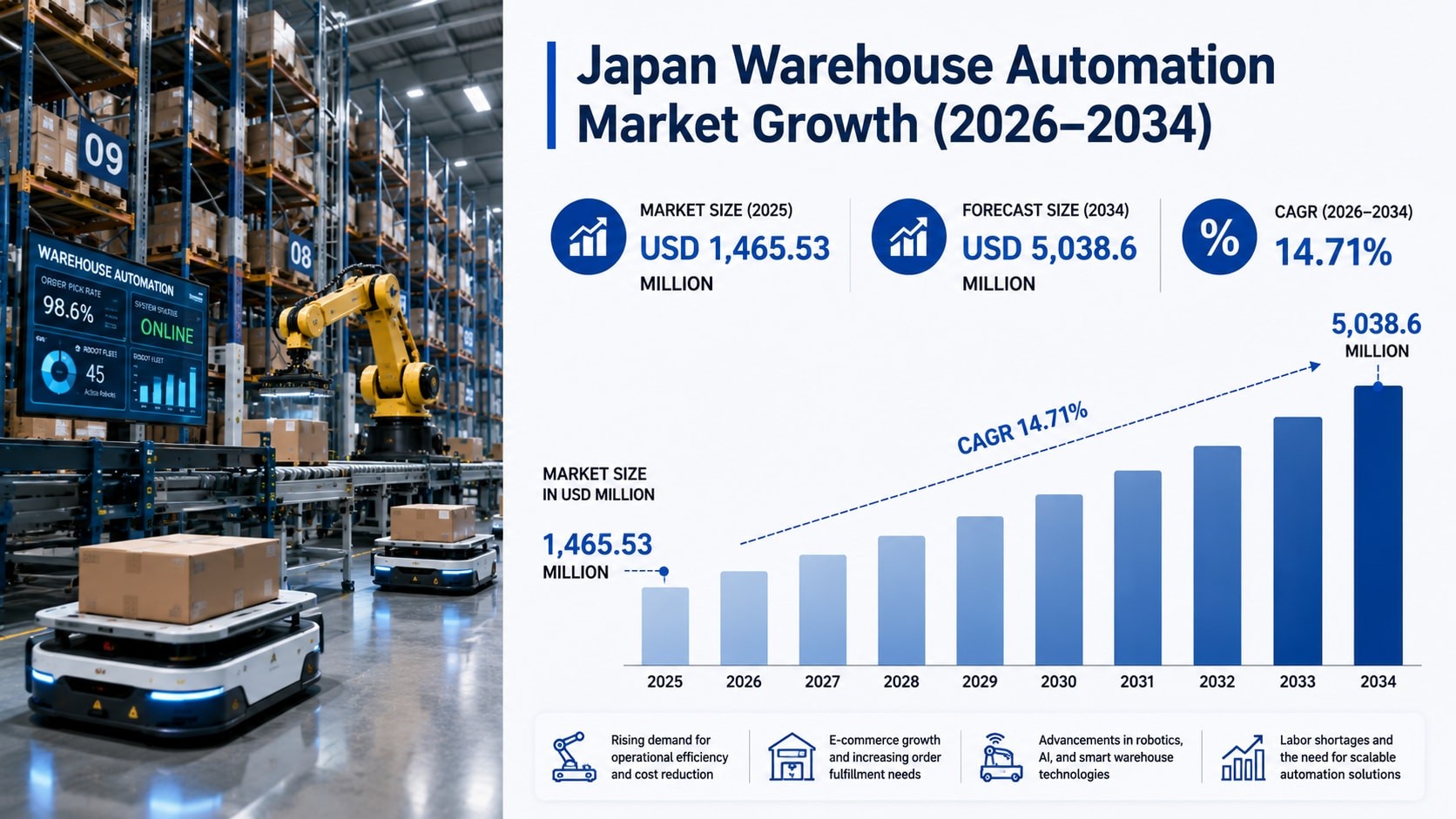

According to vocal.media, the Japan warehouse automation market size reached USD 1,465.53 million in 2025 and is projected to reach USD 5,038.6 million by 2034, growing at a compound annual growth rate (CAGR) of 14.71% during 2026–2034.

Drivers: E-Commerce, Labor Shortages, and AI Integration

Rising e-commerce activity is accelerating demand for high-speed fulfillment infrastructure. Japan’s online retail expansion has intensified pressure on logistics operators to reduce delivery lead times — a challenge compounded by a national labor shortage driven by an aging population and shrinking workforce. According to the report, automated systems are now essential for maintaining productivity amid declining working-age demographics. The source states that warehouse automation technologies directly address this constraint by reducing manual labor requirements while improving workplace safety and operational consistency.

Technological innovation is central to market expansion. Autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) are being deployed across logistics and distribution facilities to streamline material transportation. The report notes these systems enhance workflow optimization and real-time operational control. Similarly, AI-powered warehouse management systems (WMS) and warehouse execution systems (WES) are gaining traction to improve inventory visibility and order accuracy. Predictive analytics embedded in these platforms enable smarter decision-making — a capability increasingly critical for high-volume operations.

Hardware Dominates Component Segmentation

Hardware accounts for the largest share of the market, with multiple subcategories driving adoption. These include mobile robots (AGV, AMR), automated storage and retrieval systems (AS/RS), automated conveyor and sorting systems, de-palletizing/palletizing systems, automatic identification and data collection (AIDC), and piece picking robots. AS/RS solutions, in particular, are highlighted for maximizing storage capacity while boosting picking speed and inventory accuracy — especially in distribution centers handling >10,000 SKUs per day.

Software components include WMS and WES, while services cover value-added offerings and maintenance. End-user industries span food and beverage, post and parcel, retail, apparel, manufacturing, and others. Regionally, the Kanto Region — home to Tokyo and over 28% of Japan’s logistics infrastructure — leads in deployment volume, followed by the Kansai/Kinki Region and Central/Chubu Region.

Competitive Landscape and Implementation Realities

The competitive landscape includes robotics manufacturers, logistics technology providers, software developers, material handling equipment companies, and system integrators. Success hinges on technological innovation, integration capabilities, scalability, and after-sales support — not just hardware specs. Companies investing in AI-powered automation platforms and intelligent warehouse software are strengthening their market position, per the source.

From a practitioner perspective, supply chain professionals in Japan face urgent implementation trade-offs: integrating legacy warehouse management systems with new robotics middleware requires specialized engineering resources — a scarce asset in domestic IT labor markets. Maintenance service contracts now routinely include SLAs guaranteeing 99.5% uptime for AS/RS subsystems and response windows under four hours for AMR fleet failures. These contractual benchmarks reflect growing operational dependency on automation reliability.

Source: vocal.media

Compiled from international media by the SCI.AI editorial team.