According to www.scmp.com, China’s shipyards have secured at least 14 very large crude carriers (VLCCs) in recent weeks — driven by shipping disruptions linked to the US-Israeli war on Iran and the effective blockade of the Strait of Hormuz.

Strait of Hormuz Blockade Tightens Global Tanker Capacity

The Strait of Hormuz — handling about a quarter of the world’s seaborne oil — has been largely blocked for eight weeks, sending crude oil prices to historic highs and forcing tankers to take longer alternative routes. This has exacerbated existing fleet constraints caused by ageing vessels and intensified pressure on global shipping capacity.

Orders Flow to Chinese Shipyards

Three international firms have placed VLCC orders with Chinese shipyards, citing advantages including strong construction capacity, lower costs, and shorter delivery timelines:

- Advantage Tankers (Switzerland) ordered two 307,000-deadweight-tonne VLCCs from a Chinese shipyard; deliveries are scheduled for Q2 2028 and Q3 2029, according to China Ship Survey.

- Mercuria Energy Group (Geneva-based) signed contracts worth nearly US$650 million for up to four VLCCs and two LR2 product tankers, with deliveries expected by 2029, per the same journal.

- Yangzijiang Maritime Development (Singapore-based, backed by Chinese shipbuilding tycoon Ren Yuanlin) placed an order for eight VLCCs — its first entry into the large-tanker segment — with deliveries planned between 2028 and 2030, as shown in company filings.

Existing Projects Gain Value Amid Market Shifts

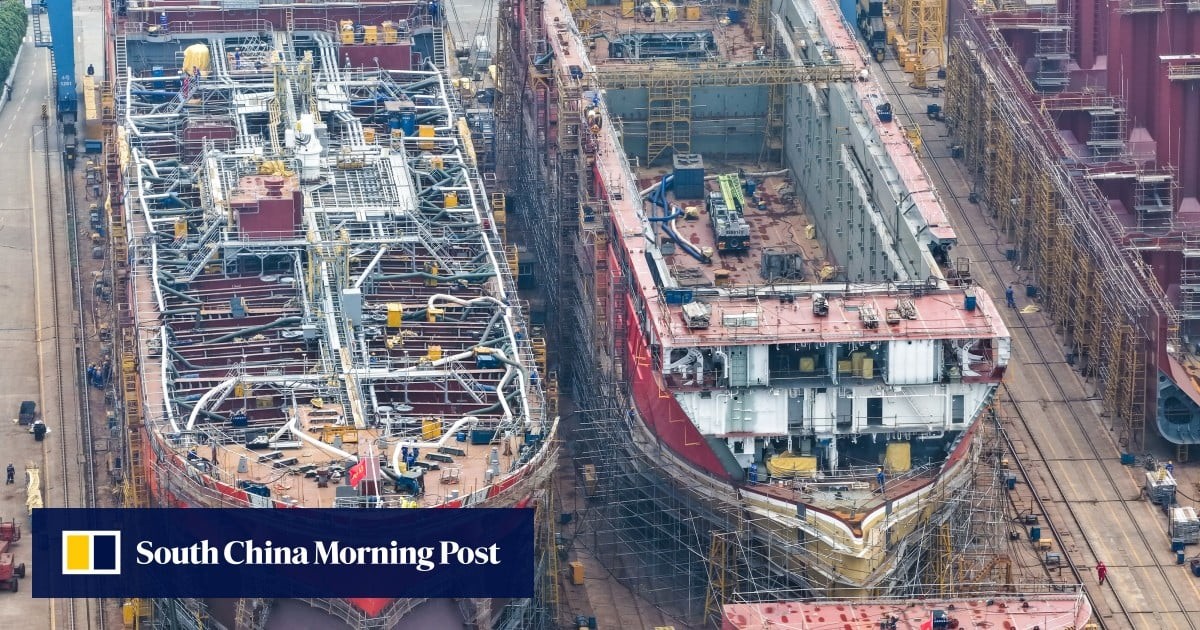

Advantage Tankers’ existing VLCC under construction — the 319,000-deadweight-tonne Advantage Visual — is being built at a Jiangsu province shipyard and is due for delivery in Q4 2026. Acquired from Trafigura for about US$119 million, the vessel is now valued at approximately US$152 million, according to China Ship Survey.

This surge reflects broader industry dynamics: China already dominates global shipbuilding orders, and geopolitical stress is accelerating client diversification away from traditional builders like South Korea. For supply chain professionals managing energy logistics, the shift signals heightened reliance on Chinese-built tonnage — with implications for lead time planning, chartering strategy, and contingency routing amid persistent chokepoint risk. The extended delivery windows (2028–2030) also underscore the multi-year horizon required to scale tanker capacity in response to acute disruptions.

Source: South China Morning Post

Compiled from international media by the SCI.AI editorial team.